Tesla 2022 Q2 Results - Implications for Chinese Renewable and EV Stocks, Part 1

Featured Stocks: Ganfeng Lithium, Tianqi Lithium, CATL, EVE Energy

Tesla’s 2022 Q2 results and earnings call are out, and there is a lot to chew on. For an abbreviated version, you can find the earnings call notes here. I will highlight some of the important items I am focused on (no, not Bitcoin, Dogecoin, or regulatory credits) and how they read through to stocks that I cover in the Chinese renewable and EV space.

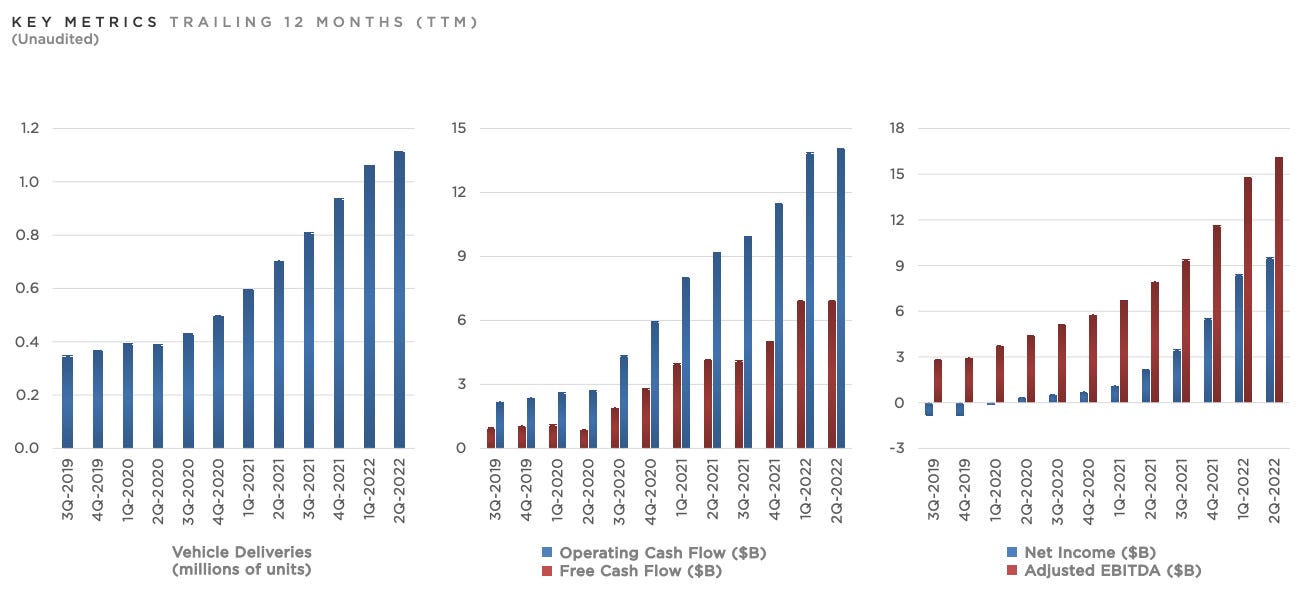

Production and delivery growth fell sequentially from Q1 due to 22 days of lost production at Giga Shanghai during the government lockdown in response to the Shanghai COVID-19 outbreak and another 40 days of running only one shift before resuming normal production. However, Tesla ended the quarter with a record month of production in June. Total deliveries for Q2 grew 27% year-over-year, still an excellent result considering the auto industry is expected to register another decline in sales for 2022.

Automotive revenue grew 42% year-over-year, as price increases drove ASP up 9.2%. Automotive gross margins were down sequentially but higher than in Q2 2021, despite less high-margin contribution from Giga Shanghai, rising commodity prices, and low volume production during the initial ramp of Giga Austin and Giga Berlin. Tight control of operating expenses enabled significant operating leverage, as operating margin expanded from 11% to 14.6% and operating income grew 88% year-over-year. Margins should recover toward Q1 highs as expanded capacity in Shanghai comes online. Given the quarterly variability that arises from one-off COVID-19 supply chain disruptions, it is also helpful to track key metrics on a rolling twelve-month basis:

Tesla’s exceptional profitability metrics, while operating at only 1/20th of the scale it plans to reach by 2030, highlight the power of vertical integration, similar to what we see with other leading Chinese renewable technology companies, such as Longi Green Energy, Pylon Technologies, CATL, and Ming Yang New Energy. Tesla is continuing to extend itself upstream toward battery cell production and raw material mining/processing, and its in-house hardware/software development and AI training capabilities are driving its downstream ambitions in Transportation as a Service (TaaS).

Lithium Refining

It is important to keep in mind that demand is not a limitation for Tesla; wait times now extend into Q2 2023 and the challenge continues to be ramping production as fast as possible. Production can only move as fast as the slowest moving part, and throughout Tesla’s history, the limiting factor to production has been the supply of lithium-ion batteries. Elon Musk specifically called out lithium processing as the fundamental rate limiter in the Q2 conference call, encouraging entrepreneurs to enter the lithium refining business and noting the “software margins” in lithium carbonate and lithium hydroxide processing are “a license to print money.”

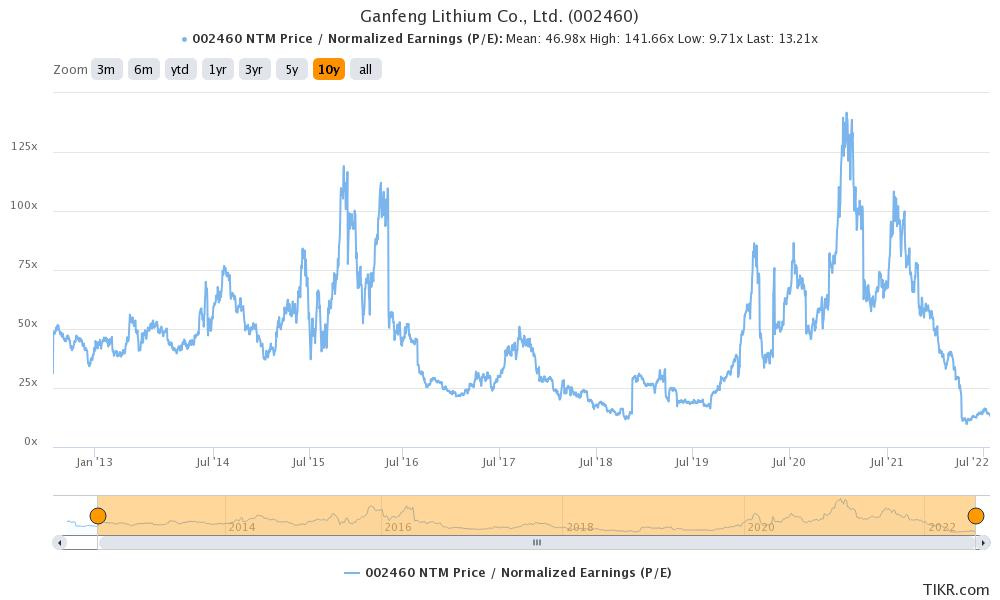

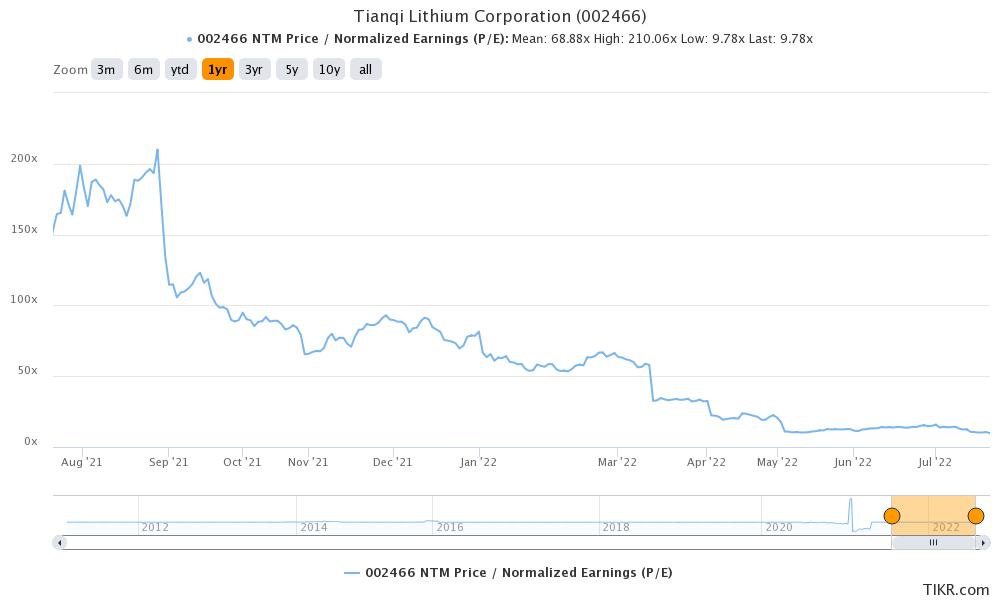

Investors interested in the lithium space should start by studying the Chinese leaders, Ganfeng Lithium (1772:HK, 002460:SZ) and Tianqi Lithium (9696:HK, 002466:SZ). Both stocks have printed money for long-term investors; Ganfeng and Tianqi’s 10-year annualized price returns stand at 43.9% and 33.1%, respectively.

Both companies are expected to print money going forward, thanks to the surge in lithium prices. Ganfeng Lithium is expected to grow revenues 250% and operating income 350% in 2022, with operating margins expanding to 40%. Tianqi is expected to register even greater revenue growth of 320% and operating income growth of 480%, with operating margins of 72%, far better than any listed software company that I’m aware of!

The huge bull run in the shares of Ganfeng and Tianqi has actually been outdone by their financial performance. As a result, the stocks’ forward earnings multiples are sitting near their all-time lows.

Ganfeng and Tianqi are not components of the TMC China Solar/Wind/Battery Index, although perhaps this is an oversight that may be corrected in the future. On the one hand, the abundance of lithium in the Earth’s crust and mouth-watering margins should attract ample competition and keep a lid on prices, and low earnings multiples on cyclical commodity producers tend to signal the top of the cycle. However, we are also still in the very early stages of total global electrification, which could require 100x more lithium annually than we mine today. Tesla has communicated its intentions to enter the market with a novel lithium clay extraction process, but the primary motivation is to accelerate industry growth and supplement suppliers, not replace them. Furthermore, Musk admitted on the call that barriers to entry in lithium refining are quite high, stating “refining of the lithium into ultra-high purity battery-grade lithium hydroxide, lithium carbonate is quite difficult and requires a massive amount of machinery and it’s a hard thing to scale.” Ganfeng and Tianqi may have already built an insurmountable lead in the most important race of our time.

4680 Batteries

The 4680 cell production ramp in Austin has been slower than some hoped, but the team sounded excited to report key progress made at their Kato Road pilot facility, allowing for 35% month-over-month production growth. Tesla has a contingency plan in place with enough 2170 cells from suppliers to meet its 2022 production goals, but unlocking 4680 mass production will be critical for production plans in 2023 and beyond, particularly for heavier vehicles like the Cybertruck and Semi. Regarding the 4680 ramp and relationship with other battery suppliers, Musk stated:

“It is not as though Tesla intends to displace our suppliers of battery cells. The Tesla battery cell production is in addition to what our suppliers can do. And we want our suppliers to grow their battery output as fast as they possibly can, and that goes for the entire supply chain. The fundamental rate limiter for both transitioning to sustainable energy is how fast can you grow with the amount of battery output per year? This is the fundamental rate limiter for transition to sustainability because you need the batteries for two of the pillars of sustainability, the stationary storage and for vehicles.”

As Tesla solves the dozens of little problems associated with scaling their revolutionary DBE (Dry Battery Electrode) technology, Drew Baglino stated on the call that “we want to bring (the learnings) back to our partners so that they can go faster, too, because that’s all part of the mission, how do we accelerate?” I think these developments and comments are very bullish for their existing battery suppliers, who are likely to continue to sustain high levels of cost reduction and revenue growth as they share learnings with Tesla and accelerate production. If the history of the lithium-ion battery industry is any guide, I think the growth potential of 4680 cells is being underestimated by the market. TMC Index components CATL (300750:SZ) and EVE Energy (300014:SZ) are reportedly planning on producing 4680 cells and their revenue growth has accelerated to triple digits in 2021 and 2022, yet analysts estimate future revenue growth will be relatively anemic in the near term, especially CATL:

The two stocks are valued at 25x-30x 2024E earnings, a reasonable valuation given their critical role in the energy transition and demonstrated ability to grow at the 50%+ compound rate that Tesla envisions. CATL and EVE are also notable given their expertise in LFP (lithium iron phosphate). Musk expects LFP or LMFP (LFP plus manganese) to make up roughly 2/3 of global lithium-ion battery supply in the long run, as iron is far cheaper and more abundant than nickel and cobalt. Baglino remarked on the call that most new battery technologies were simply not scalable and thus distracted from the mission of transitioning to sustainable energy as quickly as possible. Musk agreed:

Is some breakthrough needed in battery technology for the world to transition to sustainability? The answer is no. Even if there were zero technology breakthroughs, so literally zero from where the technology is right now, we could fully transition Earth to sustainable energy. The issue is very much the rate at which the entire supply chain from mining to refining to cell production. How fast can that grow? It’s growing fast and the faster it grows, the faster we transition to a sustainable energy economy.

Along with CATL and EVE, this is bullish for every component in the TMC China Battery Index, which hold established market positions in the lithium-ion battery supply chain and are now rapidly scaling production. As costs naturally come down with economies of scale, more demand will be unlocked.

In Part 2, I will discuss Giga Castings, FSD/Robotaxi, the EV competition in China, and Tesla’s valuation. Be sure to subscribe so you don’t miss it, and help me spread the word by liking or sharing these posts on Twitter or Linkedin!