Tesla 2022 Q2 Results - Implications for Chinese Renewable and EV stocks, Part 2

L.K. Technology, BYD, Nio, Xpeng, Li Auto

Continuing from Part 1, I am highlighting important points from Tesla’s 2022 Q2 Earnings Call and their implications for various Chinese renewable and EV-related stocks.

Giga Casting

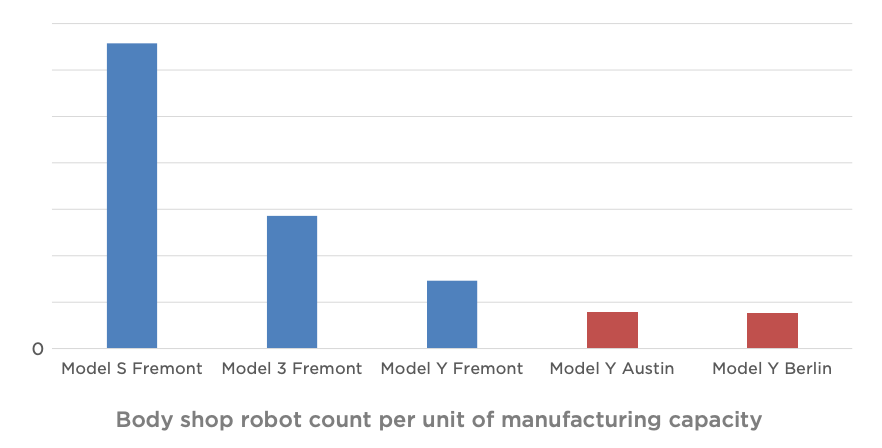

Tesla’s Q2 earnings presentation highlighted the massive improvement in body shop efficiency enabled by their adoption of large castings, which significantly reduces the number of parts and processes in assembly.

The architecture of electric vehicles allows us to rethink vehicle design and the manufacturing process beyond what was possible in the combustion engine era. Thanks to large castings and parts consolidation, the robot count in our body shops in new factories dropped by over 70% per unit of capacity compared to our first iteration of Model 3 Body Shop. Our quest for simplification is not over. We will continue to drive simplification further with every new product and every new factory.

On the earnings call, Musk noted that Tesla is making the world’s largest castings, which both improve the build quality of the vehicles and lower production costs:

We reduced body welding robot count by 70% per unit of capacity in Austin and Berlin. So that’s, call it, roughly a body shop that is roughly 3x smaller than would normally be the case. And I should say it’s also lighter, cheaper and has superior noise vibration harshness. So, it’s good on every level. But this journey is not over. We will bring another level of simplicity and manufacturing improvements with Cybertruck and future products that we are not quite ready to talk about now, but I think will be very exciting to unveil in the future.

Clearly, Tesla has gone all-in on large castings and will continue to iterate the casting process for future line upgrades and new models. All of Tesla’s front and rear castings in the Model Y are made with the “Giga Press” die casting machines supplied by Idra Group, a wholly-owned subsidiary of 558:HK L.K. Technology. Tesla is leading in the industry in their adoption of large castings for electric vehicles, and Idra is the sole supplier of Tesla’s giant die casting machines. Idra claims to be “the first company to receive production orders for 9,000-ton machines that can be used for SUV and small truck markets;” these presses are expected to be used for the Cybertruck in 2023. With Idra’s leadership position seemingly uncontested, parent L.K. Technology is positioned to benefit greatly from Tesla’s ambitious capacity expansion plans to 20 million vehicles per year by 2030, as well as the rest of the industry following Tesla’s lead in adopting large castings and the automotive market transitioning from ICE to EVs.

L.K. Technology had no analyst coverage at the time when Tesla first shared their plans to use the Giga Press on Battery Day in September 2020. The shares were extremely undervalued, and as the market figured out that Idra was Tesla’s sole supplier, the stock went on a massive run from HK$0.50 per share to HK$25 per share, a 50x gain in just about one year:

The stock still has relatively little analyst coverage with a market capitalization of less than US$3 billion, but the market now has a better grasp on the fundamental impact of the deal with Tesla. There is a growing amount of content around the Giga Press and the various benefits of giant castings, particularly from the popular Youtube channel The Limiting Factor (which I also highly recommend for learning about lithium-ion battery chemistry). Initial Giga Press deliveries have had a significant impact on the Company’s financial results, with operating income from the segment growing 50%+ year-over-year in FY2022:

The stock now has enough coverage to have forward estimates, but consensus looks very conservative, considering Tesla’s 50%+ annual production target over the medium-term, the trend of Chinese EV manufacturers following in Tesla’s footsteps, albeit with smaller die casting machines, and the rapid growth of EV adoption. Analysts are modeling a decline in annual revenue growth from 33.3% to 12.9% by FY2025, while the die casting business grew revenue 44% in FY22 and is quickly becoming the biggest driver of results going forward.

Putting the potential for big earnings beats aside, the stock is reasonably priced at 18x FY24E earnings (Hong Kong Fiscal Year ends in March). The initial excitement around the stock has subsided and the shares are trading at a much lower valuation than one year ago:

The “giga” bull case long-term is that Idra can remain at the forefront of the automotive casting industry and capture a significant amount of the value created as the inherent advantages of large castings for EVs lead to a total transformation of the typical body shop. Legacy OEMs have been very slow to adopt large castings due to inertia and massive sunk investments in their existing body shops and processes, but rapid adoption of EVs and intense competition from Chinese OEMs could force their hand. Ten years from now, we could be looking at near-100% EV adoption with production dominated by a new cast of players not weighed down by legacy assets, and the use of large castings could become the dominant industry practice. Even at 100% penetration, L.K. could continue to grow faster than the automotive market by continually increasing the size and capabilities of their Giga Press, which will be in high demand from manufacturers who want to stay ahead of their competition. In the coming years, we could see Tesla’s concept of a unibody casting machine become reality.

On the other hand, we are still in the early days of EV manufacturing, and Idra will have to fend off fierce competition in China, where its parent LK Technology currently holds about 60% share of the market for die-casting machinery across its subsidiaries. Sandy Munro, who recently toured Idra’s production facility in Italy to check out their 9,000-ton Giga Press, shared a concerning anecdote from his trip:

There is a Chinese company right now that has dozens of orders for 6,000 and 7,000-ton presses. Nobody makes an 8,000 and 9,000-ton press except for Idra. Idra is accepting orders for these; however, I was led to believe by a competitor that Idra did not have any spare capacity. That is totally wrong; that is great marketing to try and crush your competition. Idra has something like 14 or 18 orders, but I just went through their factory and said you can easily double production. The guy said “yeah, but for some reason our order book has dried up.”

While the Chinese market is always hyper-competitive and the playing field is tilted in favor of local manufacturers due to regulations that support a policy of import substitution in strategic industries, I think Idra is still positioned to succeed there. Their parent company is based in Hong Kong and has six Chinese manufacturing bases, and their key customer, Tesla, is likewise a foreign operator with a significant lead in the Chinese EV industry.

Chinese EV Competition

Musk had this to say regarding Chinese competition on the call:

The best Chinese EV manufacturer is Tesla. We are actually doing the best, thanks to our incredible team in China. But I have a lot of respect for the Chinese, our manufacturers and EV manufacturers in particular. I think they will be a force to be reckoned with worldwide. They are very – they are smart and they are hardworking. And I think anyone who is not – any company that’s not as competitive as them will obviously suffer a market share decline. So obviously, we have a lot of respect for the current companies in China and then their capabilities, yes.”

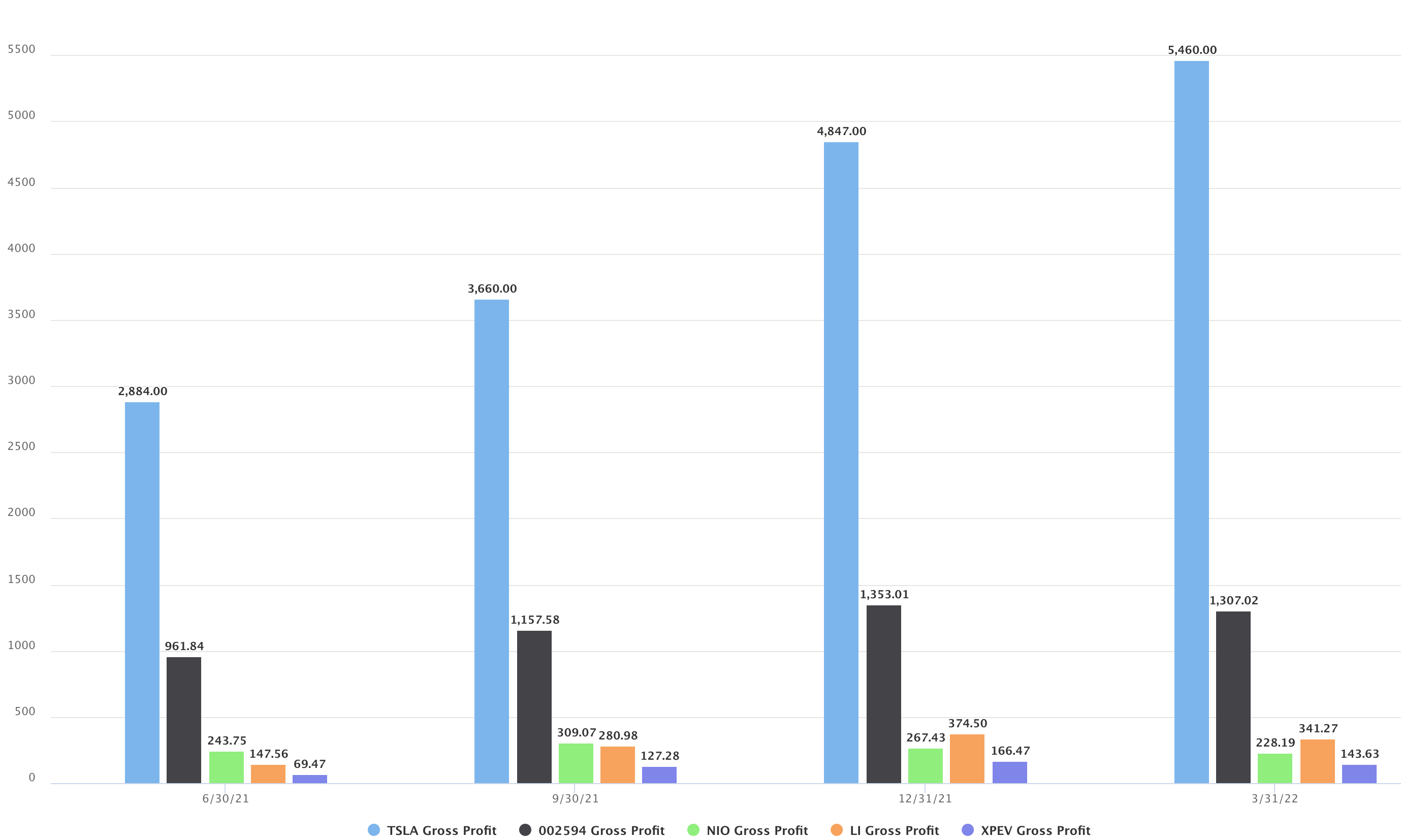

The media often cherry-picks or twists the facts to fit an alternate narrative, but Tesla’s significant lead over Chinese EV contenders is irrefutable. One simple metric we can use to measure Tesla’s lead in EV manufacturing is gross profit, which incorporates both production volume and value-added through manufacturing. In Q1 2022, two-thirds of Tesla’s global production came from Giga Shanghai. Their gross profit from Chinese production alone was about 2x the gross profit of BYD (002594), Nio, Li Auto, and X-Peng combined. Tesla’s scale and profitability advantages in EVs are even greater if we consider that a majority of BYD and Li’s profits come from hybrid vehicles, not battery electric vehicles.

Within China, the high demand for NEVs (New Energy Vehicles) is pushing out wait times as the leading Chinese EV makers are operating at full capacity. Buyers are placing multiple orders across the different EV makers and taking delivery of the first car that becomes available:

A man surnamed Cao ordered a Zeekr vehicle about two months ago and then ordered a Tesla Model 3 because he noticed that many people in some local Zeekr enthusiast groups had also ordered other brands at the same time, according to the report.

"Some group members have four or five orders in hand, and whichever order gets scheduled for production first is the one they are sure to buy," he said.

Most of the current delivery periods for NIO, XPeng Motors, and Li Auto are 2 months or less, with XPeng's delivery period reaching 3-4 months for some popular configurations, the report noted.

As the most sold NEV brand in the first half of this year, BYD's delivery period has reached nearly half a year, according to the report.

This dynamic highlights the importance of manufacturing and scaling production in the EV race; I have noted before that BYD stands out as the furthest ahead in China in terms of vertical integration and scale. BYD vehicles have yet to enter the North American market due to a 25% tariff on Chinese cars, but they are about to make a splash with new EV models in two developed markets closer to home, Australia and Japan.

The COVID lockdown in Shanghai sparked a decoupling of BYD and Tesla’s shares, with BYD rising 43% and Tesla falling 24% since Giga Shanghai was initially forced to close on March 28th. Although this “force majeure” event should have no long-term impact on the two companies’ results, BYD’s forward earnings multiple is now a 50% premium to Tesla’s:

I don’t believe this premium valuation is warranted; it will likely correct either by BYD falling or (more likely) by Tesla quickly rising back to pre-lockdown levels. Tesla has consistently outperformed BYD in terms of revenue and profit growth, yet analysts estimate that this will flip for some reason by 2024. I struggle to come up with a plausible explanation as to why this would actually happen. I think it is more likely that Chinese analysts are generally bullish on the electric vehicle industry, given their vantage point in the country that leads the world in renewable technology, including batteries and EVs. Tesla analysts are more of a mixed bag, with some traditional auto analysts who are analyzing the industry with the wrong framework, some with conflicts of interest, and even some confirmed clowns.

Given how early we still are in the EV adoption S-curve, I think it is highly unlikely that Tesla’s growth decelerates to 20% in 2025. The entire market should still be growing at a 40% to 50% annual rate by then, and Tesla’s minimum delivery growth target is 50% for the next several years. On top of underestimating the EV industry’s growth and perhaps deliberately misunderstanding Tesla’s role in it, the consensus numbers clearly ascribe no value to their Full Self-Driving software, which is very close to wide release and could also enable commercial robotaxis within the next several years. Tesla shared some key data points around the FSD Beta program in their Q2 call, which I will cover in the next installment. Be sure to subscribe so you don’t miss it!

Great analysis and write up. Will you also look at companies like Matthew’s international working on the 4680 battery via their subsidiairy Saueressig . They are a similar construct like Idra and LK