Can Tesla Compete in the Chinese Robotaxi Market?

Exploring the Chinese Autonomous Driving Landscape, including: Tesla, Baidu, Pony.AI, Nio, Xpeng, Li Auto, BYD, Zeekr, Nvidia, Mobileye, Horizon Robotics, Huawei, Xiaomi

The Money Corner newsletter brings you investable insights into the Asian markets, by telling untold stories that pique your curiosity, support your research process and help you uncover winning stocks.

This is a continuation of a series of posts highlighting the important takeaways from Tesla’s 2022 Q2 earnings report and their implications for various Chinese renewable and EV-related stocks. If you’re just tuning in, be sure to check out Part 1 and Part 2, and please subscribe!

FSD Beta Update

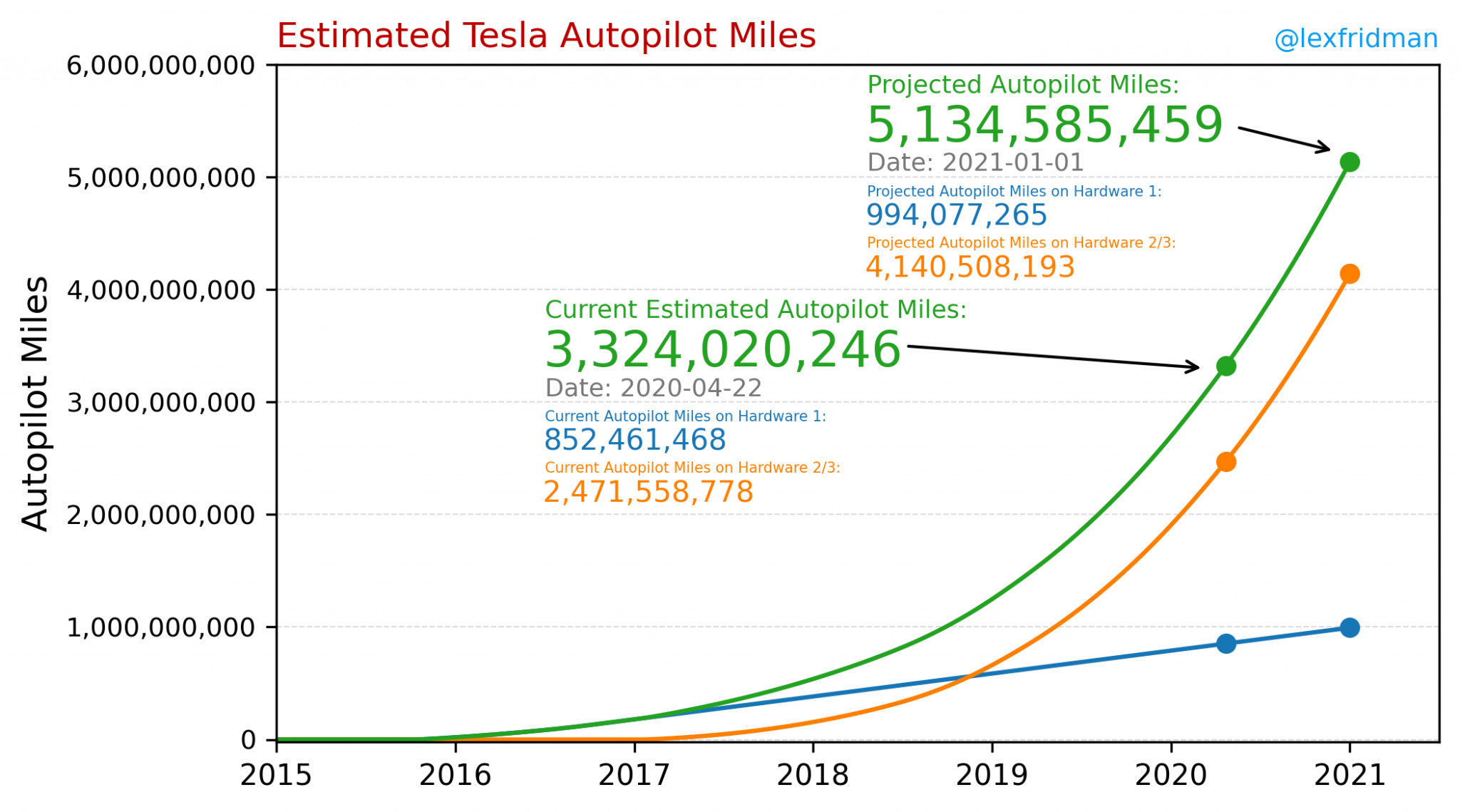

In the 2022 Q2 shareholder deck, Tesla disclosed the cumulative miles driven with FSD Beta for the first time. At the end of June, cumulative miles driven exceeded 35 million, and the software was deployed to over 100,000 owners, a 67%+ increase from the 60,000 owners in the beta program announced in January. On the Q2 earnings call, Elon Musk speculated that this number of autonomous miles driven “might be more than all other companies combined.” The chart appears to indicate that this number is growing at roughly 100% quarter over quarter, and this extreme exponential growth is set to continue as the program is expanded to roughly 1 million owners by the end of the year.

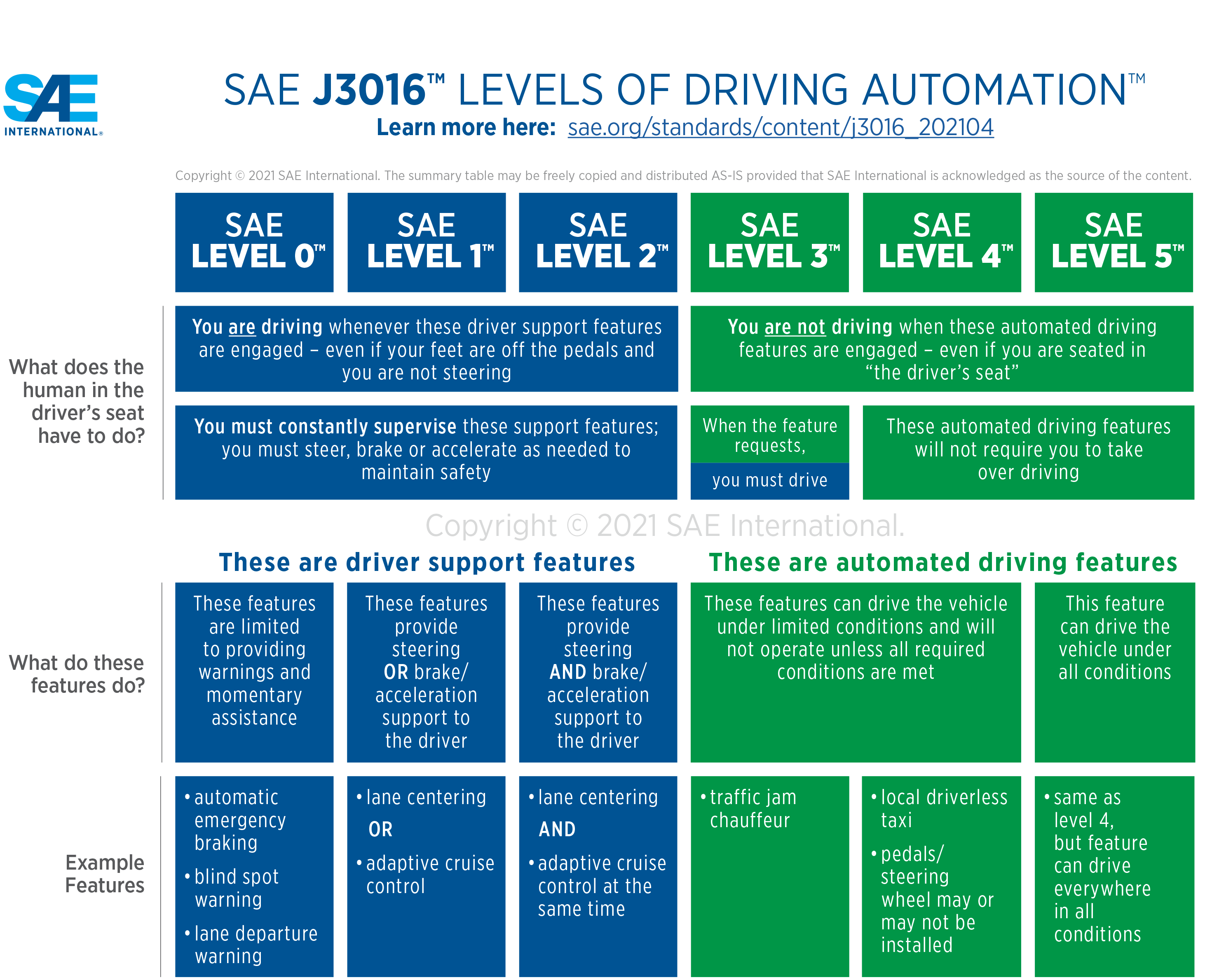

As usual, Musk’s comments require a bit more context. 35 million miles is certainly not more than competitors have logged globally, as Waymo had already logged 20 million miles by the end of 2019, Chinese autonomous driving leader Baidu Apollo announced in March 2022 that they had surpassed 15.5 million cumulative miles, and runner-up Pony.ai had driven 6.8 million miles as of April 2022. Some will also take issue with the definition of autonomous miles, as U.S. regulators consider FSD a Level 2 driver assistance system while the leading competitors have dedicated robotaxi platforms that are considered L4 systems.

However, I would advise my readers not to get too caught up with Musk’s notorious tendency to get ahead of himself, because the reality here is undeniably positive for Tesla. Tesla’s FSD beta miles logged in Q2 likely did exceed all competitors combined in North America, but more importantly, Tesla’s fleet advantage will enable them to maintain an exceptionally high rate of growth in cumulative miles driven for the foreseeable future. This is the critical input for Tesla’s success because its autonomous driving system improves as it is trained by real-world data. Tesla’s U.S. fleet capable of running FSD stood at about 1.3 million cars at the end of Q2 and is expanding at roughly a 50% annual rate. This means Tesla has a pool of 17+ billion and growing annual fleet miles to gradually tap into with no need to hire test drivers, whereas Waymo and others are physically constrained by the capital requirements and logistical challenges to ramp production of highly complex vehicles with manufacturing partners from nearly zero, as well as the need to hire qualified engineers as test drivers. GM’s self-driving unit Cruise recently disclosed that they were burning $5 billion annually to this end, shining a light on the long road of losses still ahead for those who choose to take it.

Tesla Vision vs. LIDAR

Waymo and Cruise’s approach using LIDAR and high-definition maps also presents its own scaling challenges, as the approach is more data-intensive, requires more expensive hardware, and severely limits the system’s area of operation. Former Director of AI at Tesla Andrej Karpathy explained the difference in Tesla’s approach as follows (I highly recommend all of his talks on Youtube as a starting point for understanding FSD):

I think the critical point to make is that it looks the same, but under the hood it’s completely different in terms of the approach that we take toward full self-driving. So in particular we take a heavily vision-based approach. Everyone else has a LIDAR on top of the car, the LIDAR shoots out lasers, and creates a LIDAR point cloud map. And then you pre-map the environment that you’re going to drive, so you have a high-definition LIDAR map, and you localize to it to a centimeter-level accuracy, and then you know exactly the path you’re going to take so you can just steer to keep yourself perfectly localized in the correct region. This is quite helpful, but this is not the approach that we take. We do not have LIDAR on our cars… it’s all camera-based, and we do not build high-definition maps. So when we come to an intersection we encounter it basically for the first time… how many lanes are there, which way should I turn, what are the traffic lights, which lanes do they control, all this is just done from camera vision alone. And so this is a bit of a harder problem, but of course once we actually get this to work, we can also deploy it to the millions of cars that we have globally.

Regulatory designations are hardly important in relation to a system’s actual capability and rate of improvement at this early stage in the industry’s development. The current status of FSD is reminiscent of the early days of Autopilot, which saw cumulative miles grow from 47 million miles in April 2016 to 1 billion miles in November 2018. By that point, Autopilot was roughly 6x safer than an average human driver on the highway, and it improved further to 8x as of Q4 2021.

To Wall Street, achieving autonomy is not seen as a given, and there is constant debate about the definition of autonomy, the probability of success, the timing of achieving it, and how much of the value of autonomy is priced into Tesla’s stock. To Musk, achieving full autonomy is not an option but a necessity for survival. In a recent interview, Musk asserted that solving full self-driving is “the difference between Tesla being worth a lot of money and being worth basically zero.” And no, this does not mean Musk thinks that Tesla might be a zero; in the same interview he claims “Tesla is actually going to be in a situation where Tesla has a self-driving solution and no one else is even close not even for five years.” “OK,” you may be thinking, “so the probability of success is 100%… but what does he mean by full self-driving, when do we get it, and what does it mean for Tesla’s stock price?”

Achieving full autonomy means that a car should be consistently able to travel from any point on the map to any other without the need for human intervention, more safely than the average human driver. Just as computers have replaced human operators in other manual tasks with more precision and accuracy over time, it is inevitable that computers will eventually take over the task of driving. We drive our cars using our two eyes on a swivel for input, which is processed by our brain, a biological neural net trained in the ways of the road over a lifetime of driving or riding in cars, which sends output for controlling the car via our hands and feet. Modern hardware and software should theoretically be able to reach superhuman levels; cameras, radars, and LIDAR capturing 360 degrees of the environment around the car at all times, increasingly powerful computer chips that never get tired or distracted, and high latency output that bypasses the need for physical pedals or a steering wheel, and software that gets better with training on data from an entire fleet of vehicles. All self-driving systems have these basic elements, but Tesla’s system has unique characteristics that collectively should give it an edge in achieving full autonomy first.

Tesla uses camera vision and neural nets to stitch together a bird’s eye view of the road in combination with GPS for the car to navigate its environment, rather than cross-checking pre-loaded HD maps with LIDAR input. This makes it possible for their solution to work from any point to any point, while reliance on LIDAR means competitors can only operate within predetermined ring-fenced locations. Ring-fencing severely limits the utility of a self-driving system; riders may be able to take short trips in dense urban areas but unable to commute to work from the suburbs. While LIDAR is useful for measuring distances to objects, Tesla patented a process for using image data to measure distance, effectively eliminating the need for the additional expensive, power-hungry, and obtrusive hardware. Over time the vision-based system should improve to be just as effective as LIDAR or radar, as we don’t need to shoot lasers out of our eyeballs to estimate the speed and distance of objects in our field of vision! At the same time, it should exceed a human driver’s ability to react to their environment due to the additional cameras pointed in all directions at all times.

Neural Net Hardware and Training

Another unique aspect of Tesla’s system is that it uses self-designed chips to drive and train its neural nets in the data center. Tesla’s FSD Chip, which entered development in 2016 and was introduced to the public at Autonomy Day in 2019, was a masterstroke of semiconductor engineering. The chip was the first ground-up neural network accelerator designed explicitly for the task of driving, a significant departure from other systems repurposing GPUs designed for general purpose solutions. The FSD Chip delivered far superior performance in terms of operations per second to Tesla’s previous hardware stack and competing solutions, while lowering the cost of the parts that could be retrofitted into existing cars and consuming a small fraction of the power. At AI Day in 2021, Tesla introduced Dojo, hardware designed specifically for training neural nets in the data center with the intention of replacing their massive clusters of GPUs. Again, Tesla shocked the industry to the point of disbelief with their ability to quickly develop a superior solution with an elite in-house engineering team and deliver huge performance gains over incumbents.

Aside from the performance to be gained from designing tailor-made compute hardware for self-driving, Tesla is significantly reducing their costs by sidestepping NVIDIA’s GPU monopoly. Last fiscal year, NVIDIA reported gross margins of 65% on nearly $27 billion of revenue. As Tesla scales car production and its data centers, it will eventually save billions, perhaps even tens of billions of dollars each year that would otherwise go to NVIDIA’s bottom line. If you are looking to win friends and influence people, maybe don’t rub this point in if you ever happen to meet any $META bag… um, investors.

In addition to its hardware advantages, Tesla has a distinct advantage in collecting training data from real-world miles. Tesla recently sold its 3 millionth car globally and is expected to exit 2022 on an annual production run rate of 2 million cars. That means Tesla can access tens of billions of miles per annum of real-world data for neural net training across a wide geographic area. More data means more quality data, such as rare road events that would be difficult to simulate. Building out a fleet this size equipped with the hardware necessary for collecting training data and also capable of self-driving is a difficult chicken and egg problem, and it remains to be seen if any other company will be able to crack it. Other “leading” self-driving operations in the U.S. currently have fleets in the hundreds.

Tesla’s hardware and fleet advantages are very important because the amount of compute available and the size of the dataset are the key constraints to training and improving neural nets. There is nothing that unique about the deep learning algorithms Tesla uses to train neural nets, as these have been widely known and agreed upon in the industry for some time. Human ingenuity is also becoming less relevant in updating the self-driving software code, as the original “1.0 code” written by humans is being gradually replaced by “Software 2.0,” which is machine-written code coming out of the neural net training process. In this new paradigm, software engineers working on FSD at Tesla are spending most of their time curating datasets rather than writing code. Tesla’s fleet enables engineers to source mispredictions from the neural nets at scale, which are then labeled correctly and put in a dataset to retrain the neural nets.

As the process of collecting data from the fleet, labeling it, retraining the neural nets, and rewriting software code becomes increasingly automated, Tesla is building a formidable flywheel that will accelerate their own progress in self-driving and make it very difficult for others to catch up. More cars on the road will make their software better which will in turn increase demand for their cars. According to Karpathy, there is no upward bound on the performance of the neural nets, so eventually FSD will attain superhuman ability… and still continue to improve.

WEN ROBOTAXI?

There’s no denying that FSD and robotaxis are late. Musk has promised Level 5 autonomy within 12 months every year for the past nine years, which gives his critics plenty of easy ammo and has lulled the market into not giving Tesla any credit at all for future robotaxi domination. However, now that the pieces are in place (superior hardware, fleet scale, neural net training cycle) and miles driven are on a steep exponential curve, the system could very rapidly improve to become safer than a human driver. Some FSD Beta testers have been reporting significant improvements in the latest builds with frequent zero-intervention drives, but this anecdotal data is not sufficient to gauge progress. I think the market will need to see the progression of miles per intervention or accident rates, data that Tesla is keeping close to its chest, in order to start factoring the potential of robotaxis into the present valuation of the stock. My confidence that we will reach that point eventually and then suddenly comes from studying other deep learning curves, such as AlphaGo Zero. Starting from scratch as the worst Go player in the world, AlphaGo reached world champion ability after only 36 hours of training. Self-driving is a far harder problem to solve than placing stones in the right place on a Go board, but the principles of deep learning are the same.

Given the steep learning curve enabled by Tesla’s neural net training flywheel, FSD could indeed work as advertised with a high rate of reliability by the end of this year. However, regulatory approval will lag self-driving ability, with the speed of approval depending on the jurisdiction, test mile rate, and safety record. In North America, Waymo and Cruise are nearing paid passenger rides in San Francisco, and Baidu recently announced approval to charge passengers for driverless rides in Wuhan and Chongqing. For localized solutions using LIDAR and HD maps, testing in a relatively small area and negotiating with local officials is the only way forward, but this will be tedious and expensive to scale. Tesla does not seem to even be pursuing these city-level regulatory approvals; it is likely to focus on broad regulatory approval at higher levels after logging far more miles. In his 2016 Master Plan, Musk stated “we expect that worldwide regulatory approval will require something on the order of 6 billion miles (10 billion km).”

FSD Cumulative Miles Driven Model

FSD Beta drivers are logging about 7 million miles per month at present, which amounts to only about 2.3 miles per driver per day across 100,000 drivers. This is low compared to the average mileage driven in the U.S. of 30+ miles per day, but it actually represents a fairly high usage rate considering most miles are driven on the highway and FSD Beta is currently only for city streets. A combination of FSD and Autopilot into a single software stack is planned for the near future, which would substantially increase miles driven per day on FSD. I assume drivers who have purchased FSD are also more likely to be heavy Autopilot users, accounting for more than the estimated ~5 miles per day of Autopilot usage across the entire fleet. Heavier usage could also be encouraged via lower insurance premiums from Tesla in states where they are licensed to operate. Assuming a wide release to 1m drivers by the end of 2022 as guided on the Q2 call, a gradual increase in uptake and usage as the system improves, and a continued ramping of global production in line with management guidance, cumulative miles driven on FSD should continue to grow exponentially, crossing the 10 billion mile mark at some point in 2024 or perhaps early 2025:

As for safety, some deaths and accidents will be unavoidable, but the important statistic to focus on is the rate. In 2021, 1.34 traffic deaths were recorded for every 100 million vehicle miles traveled in the United States. Extrapolating Lex Fridman’s estimates from April 2020 based on actual delivery numbers, cumulative miles traveled on Tesla’s Autopilot has now likely exceeded 11 billion miles. Thanks to accidental bull Ed Niedermeyer’s Tesla Deaths website, we know that there have been 15 confirmed deaths on Autopilot in its history, which amounts to 0.136 deaths per 100 million vehicle miles traveled, a 90% reduction from the average rate. Teslas have also proven to be significantly safer than the average car without Autopilot, with 290 deaths total over an estimated 73 billion miles, or 0.40 traffic deaths for every 100 million vehicle miles. If FSD’s safety record can match Autopilot's over 10 billion miles, it would be a strong validation of Tesla’s alternative approach to self-driving and likely pave the way for regulatory approval for robotaxis across the United States. As most of the automotive fleet becomes autonomous, traffic deaths will become extremely rare events, something to look forward to for future generations.

Regulatory approval of FSD in late 2024 would coincide with Musk’s recent guidance for robotaxi entering mass production at Giga Austin in 2024. The unit economics of a mass-produced electric robotaxi, unencumbered by geographical ring-fencing would be extremely attractive, but even the financial implications of just delivering FSD are huge. At current prices in the U.S., adding 1.5 million drivers in 2024 would mean between $18 billion of one-off 100% gross margin revenue and $3.6 billion of recurring subscription revenue with a higher lifetime value. This potential bonanza, for the most part, is not factored into Wall Street’s forward-looking financial model. Not only does the consensus analyst estimate forecast a sharp deceleration in revenue growth despite the Company’s 50% annual production growth guidance, but EBITDA margins are also expected to stay roughly flat, implying no significant boost from an increase in high-margin FSD sales.

Continue to Part 2 for a Tesla Robotaxi financial model and an overview of the Chinese autonomous driving landscape.