China Renewables Round-up 2022.07.11

Index Performance vs. Benchmarks

The TMC China Solar/Wind/Battery Index rose 1.2% from June 30th, outperforming the CSI 300 (-1.1%) and the U.S. Energy sector ($XLE -0.8%).

Notable Moves

688063 Pylon Technologies +28.8%

The world’s second-largest consumer energy storage provider (after Tesla) stands to benefit as the hot European market gets even hotter. European household storage is expected to exceed 4 GWh in 2022, an increase of more than 150%, as sharply rising electricity prices increase homeowners’ yield on investment. Pylon enjoys high barriers to entry due to long-standing distribution partnerships with leading PV energy storage system providers, and sales are expected to reach 3.1 GWh in 2022, a 105% increase year-over-year. The Company is expanding production capacity in phases to 17 GWh by the end of 2025.

300073 Beijing Easpring+15.7%

The supplier of cathode materials for lithium-ion batteries forecasted an increase in H1 net profit of 101-124% from a year earlier, exceeding market expectations and triggering a series of upwards earnings forecast revisions. The Company is shipping a larger proportion of high-nickel cathode material, which is improving overall profit per ton. The Company also launched an equity participation plan for management and employees.

Corporate Actions

300014 EVE Energy issued a 0.16 CNY Cash Dividend on July 8

300861 Yangling Metron New Material issued a 1 CNY Cash Dividend on July 7, as well as a 1.2:1 Stock Split

Industry News

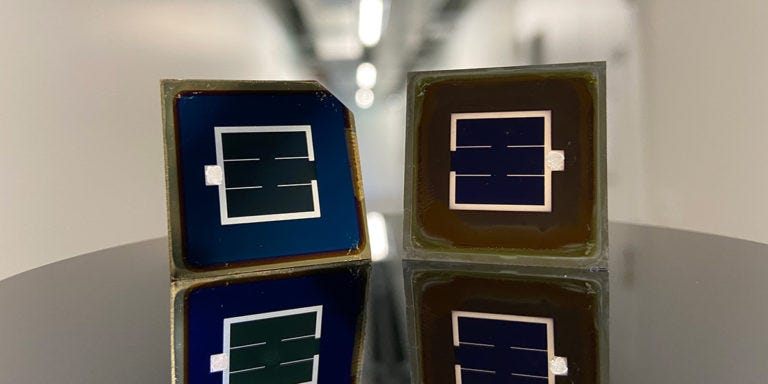

Scientists have broken the efficiency record for tandem silicon-perovskite solar cells, exceeding the 29.4% theoretical efficiency limit of silicon alone. The progress being made with tandem cells at lab scale suggests that the solar PV learning curve will continue well beyond 2030.

JinkoSolar commissioned a 20GW n-type ingot fab in Qinghai province. Rapid adoption of n-type monocrystalline silicon wafers would be very positive for top pick KBC Corporation.

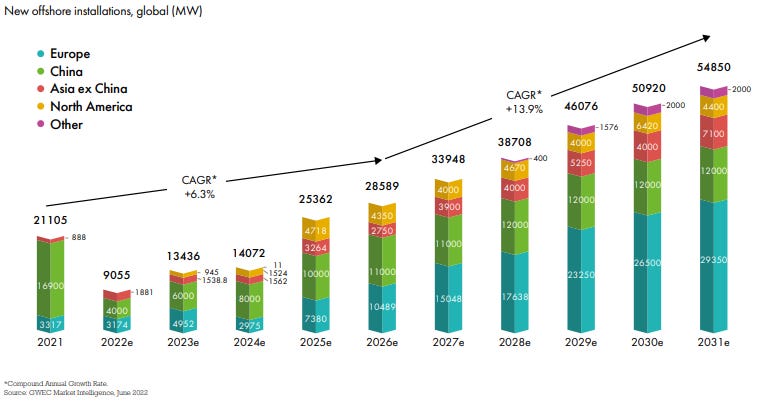

The Global Wind Energy Council released their 2022 Global Offshore Wind Report. The internet has been buzzing about the potential of offshore wind as the price of offshore wind power in the UK fell to an all-time low in a recent auction. The TMC China Solar/Wind/Battery Index has two components that will benefit greatly as offshore wind reaches grid parity in China, which we will explore in more depth in future articles.

As the 2022 Q2 China EV sales are tallied, the headlines have been a bit ridiculous. Major media outlets are cheering BYD’s apparent rise to the top of the global electric vehicle industry, conveniently ignoring several facts. One, the term “electric vehicles” is being used as a catch-all term to include plug-in hybrid vehicles, which attach a much smaller (~15kWh) battery to a gas engine. Two, Tesla’s production was stalled for nearly two months as Giga Shanghai was closed during the recent COVID lockdowns in China. And three, BYD’s battery electric vehicle deliveries on average have a much lower ASP than Tesla and include smaller cars for the Chinese market with smaller battery packs and lower range. If we look at Battery Electric Vehicles alone, Tesla still held a comfortable lead in Q2 despite significant production challenges, and in June the Model Y was the best-selling model of all vehicle types in China, despite having an ASP higher than the next five best-selling cars combined. That being said, BYD is a component of the TMC China SWB Index as it is the largest Chinese battery electric vehicle maker, notable for the extent of its vertical integration in battery design and manufacturing.