Top Pick: KBC Corporation

Dominant supplier to the solar industry rapidly expanding into new markets

Elevator Pitch: KBC Corporation has a large cost and quality lead in supplying consumables used in the monocrystalline silicon wafer production process, counts all major players as customers and is gaining market share as fast as it can expand production capacity. Sales tripled in 2021, and the company enjoyed 40% EBIT margins. Expected technology trends in the solar industry are very favorable for continued robust growth in its core market, and the Company is now leveraging its advantages to enter new markets, which have the potential to exceed the size of its existing markets. Despite a 200%+ return following its IPO two years ago, the stock is still under the radar as it has one of the smallest market caps in our indices. It trades at an FY24E P/E of 20x, and earnings growth has the potential to outperform analyst expectations for about 35% annually over the next two years.

KBC Corporation (688598), founded in 2005 in Yiyang, Hunan, designs and manufactures carbon-based composite materials and products. Its core products are consumables used in monocrystalline ingot pulling furnace hot zones (thermal fields), including crucibles, reflectors, shields, heaters, rings and electrodes, as seen in the diagram below:

As we know from studying Longi, monocrystalline silicon wafers have replaced polycrystalline silicon wafers for good as improvements in the production process have brought down costs and improved cell efficiency. Increasing crucible capacity was one driving factor in enabling more efficient production of larger silicon ingots. The vast majority of solar cell production going forward will use monocrystalline silicon wafers, and the industry is rapidly expanding production capacity across the supply chain to meet booming end-user demand for solar modules, practically ensuring growth in new demand for equipment related to the monocrystalline production process. KBC is growing significantly faster than this market, for several reasons.

One, carbon-based composite materials are expected to fully replace imported isostatic graphite products for furnace thermal field applications given advantages in strength, heat resistance, and customization. The market for carbon composite thermal field materials grew roughly 30% and penetration crossed 60% in 2021.

Within the carbon composite thermal field market, KBC is recognized as the clear cost and quality leader, with a 1-2 product generation lead over its nearest rival, Xi’an Chaoma. KBC has several key advantages over competitors, namely its independent design capabilities for customized production equipment, the ability to make carbon fiber preform structures in-house (~40% reduction in raw materials cost), and a novel single carbon source rapid chemical vapor deposition process which shortens the densification cycle by more than 50% compared with peers, which greatly reduces power consumption and improves production efficiency. KBC’s control of the entire process also enables higher-purity products, which unlocks higher value markets.

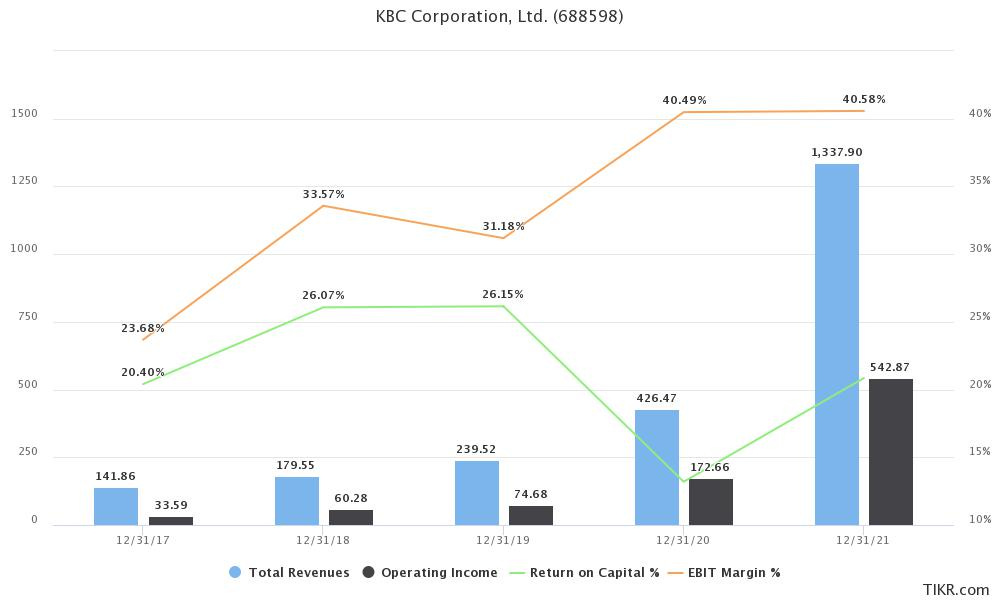

With unit costs less than 40% of Xi’an Chaoma and falling at a faster rate, KBC has been able to maintain gross margins above 50%, despite consistently falling product prices and an 18% increase in carbon fiber raw material in 2021 (expected to decline again in the near-term as new capacity comes online). A 200%+ increase in sales in 2021 offset a slight decline in gross margins, and the Company achieved a record EBIT margin of 40.6%. To date, KBC’s sales expansion has been primarily limited by production capacity, with all major wafer producers, including Longi, entering agreements with KBC to reserve production in advance. KBC’s unmatched dominance in its field seems to be setting the stage for a near-monopoly, and market concentration is already much higher than other parts of the solar supply chain. KBC’s market share in crucibles exceeds 35%, and share is catching up in other products as penetration of carbon composite materials increases.

The Company has a history of exceeding production capacity growth targets and maintaining a very high utilization rate. Some data points, gleaned from analyst reports:

2017 - 110 tons per year, utilization 95%+

2019 - 202 tons per year, utilization 95%+

September 2020 - 280 tons per year, 550-ton expansion planned for 2021 and 600 tons for 2022, 1,430 tons per year in total

End 2020 - 400 tons per year, 1,200 tons per year by end of 2021, 1,550 tons by end of 2022

End 2021 - 1,600 tons per year, utilization rate 105%+, 1,950 tons per year total completed in 2022

May 2022 - 570-590 tons shipped in Q1, 2,600 tons capacity by end of 2022, 3,450 tons capacity in 2023

The current capacity target of 3,450 tons in 2023 would enable KBC to address about 50% of the entire market demand for monocrystalline furnace thermal field equipment. It remains to be seen if customers will eventually set a hard limit to supplier concentration for thermal field equipment, or if KBC will be allowed to take the entire market with cheaper and higher quality products that maximize their customers’ profits.

Looking forward, renewal, replacement, and renovation demand for thermal field products are also benefitting from downstream technology trends such as increasing penetration of larger wafers and the imminent transition from p-type PERC cells to n-type HJT cells. Higher efficiency n-type HJT cells require higher purity silicon wafers, which the wafer manufacturers cannot achieve without upgrading to high-purity furnace thermal field equipment. KBC’s advanced chemical vapor deposition technology is advantageous here, as fewer impurities are introduced during the densification process. Given the higher technical specifications, customers are also implementing a lengthier and stricter supplier verification process for n-type thermal field products. With an expected 5-10% increase in cost but a 10-15% increase in price, n-type thermal field products could be a higher value and margin business for KBC with even higher barriers to entry. Only 200 tons of KBC’s current production capacity of 1,750 tons is n-type compatible, but KBC’s current expansion of 1,500 tons to be completed in 2023 is n-type compatible. As we saw with Longi accelerating the shift from polycrystalline to monocrystalline silicon wafers, KBC could accelerate the shift from p-type to n-type faster than expected, by removing the production bottleneck and lowering the cost of high-purity furnace thermal field equipment. In Q1 2022, KBC shipped 20 tons of high-purity products.

In the long run, the monocrystalline furnace thermal field equipment business will be just one pillar of KBC’s larger ambition to build an advanced carbon-based material industry platform. To date, the Company has made significant progress in the development and commercialization of products for semiconductors, ceramic brakes, hydrogen fuel cells, and carbon paper. Recent developments include:

April 11, 2022 - KBC signs 5-year strategic cooperation agreement with Bejing Tianke Heda, which is engaged in the production of silicon carbide. The company is one of three Chinese companies leading the localization of the silicon carbide market, which is expected to grow at a 25% CAGR to reach $1.7B in 2026. The market is currently 98% supplied by imports. Tianke’s production process also involves crystal pulling furnaces that require high-purity thermal field equipment.

June 6, 2022 - GAC Aion (Guangzhou Automobile) selects KBC as a designated supplier of carbon-ceramic brake discs. Sales could reach several hundred million RMB by 2023, domestic market size could reach RMB 14 billion by 2025, assuming 20% penetration. Carbon-ceramic brakes are key to weight reduction in electric vehicles, as each unit of weight savings below the suspension system has the same effect on vehicle range as five units of weight above the system. Carbon-ceramic brakes can therefore extend the range of a typical EV by about 25 km. Imported ceramic brake systems cost 80,000 RMB per car, KBC is at about 10,000 RMB per car, and cast iron brake discs are at 1,000-2,000 RMB per car. At scale, KBC should be able to reduce its price to below 5,000 RMB per car.

June 9, 2022 - KBC announces strategic cooperation with Shenli Technology to jointly develop carbon paper used in hydrogen fuel cells. The carbon paper market is currently dominated by Toray of Japan and SGL of Germany, but prices are high and import volumes are limited. KBC is building an initial production capacity of 300,000 square meters per year for commercial production by the end of 2022, and the price is expected to be more than RMB1,000 per square meter. The annual demand per truck is estimated to be about 25 square meters. The jury is still out as we wait for the mass production of an autonomous Tesla Semi, but if hydrogen fuel cells are to play any significant part in the energy transition going forward, this could be a significant business for KBC.

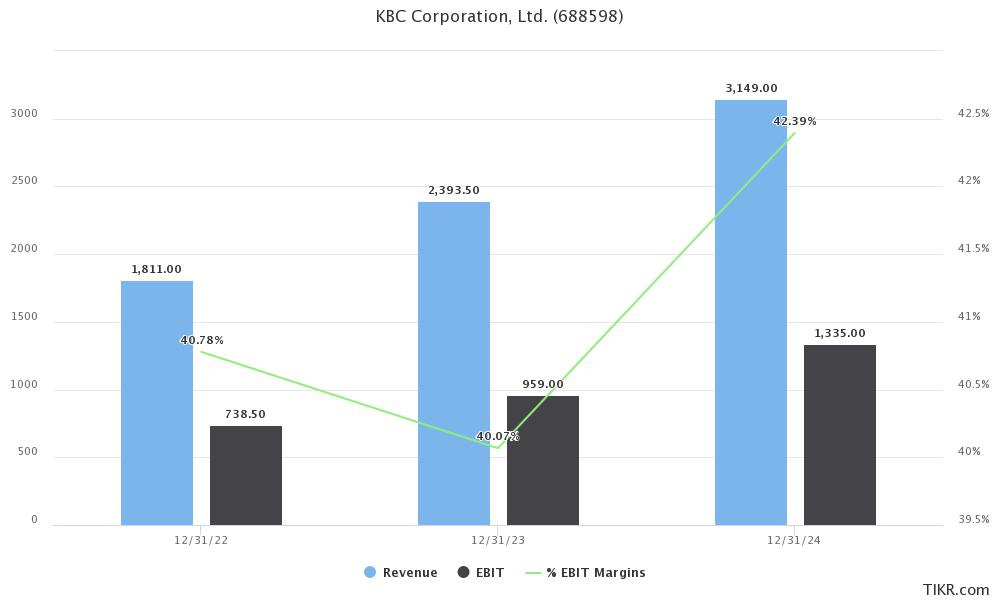

Analysts estimate KBC will grow EPS by 34% from 2022 to 2024, putting the stock at 36.5/28/20 times 22/23/24 earnings. This looks conservative, considering the Company’s planned expansion of thermal field equipment production and the potential for significant revenue generation in additional segments by 2023. Q1 2022 revenue was RMB 450 million, so current analyst estimates assume no further growth this year.

KBC’s corporate governance is similar to Longi, and perhaps a pattern will emerge across the TMC index. KBC’s core executives met at Central South University in Hunan, where they were experts in powder metallurgy and other related fields. Management is both hands-on, with relevant technical and industrial expertise, and aligned with shareholder value creation, as the company’s largest shareholders. The Company has implemented two phases of equity incentives since listing in May 2020. Convertible bonds have been issued to fund capacity expansion, which has been very accretive to EPS to date. In a very encouraging move, management decided to repurchase RMB 80-100 million worth of shares earlier this year to offset the conversion of some of the convertible bonds, with a price cap of 300 RMB per share. I think this will work out to be a good move for shareholders, looking back several years from now.

In summary, KBC’s competitive moat is one of the strongest I’ve seen in the solar industry to date, with a wide gap between its nearest competitors in terms of quality, cost, and margins. The shares are reasonably priced, management is aligned with shareholders, and business is booming. The Company is perfectly positioned to benefit from the technological roadmap of the solar industry at large, and its advantage in manufacturing carbon-based materials is unlocking new growth markets. The stock is one of my top picks in the Chinese renewable tech sector.

Hi will. Great article and they really do have room for further expansion. The stock is in the SSE Star Market, which is restricted to institutional professional investors only outside of China. Do you know how retail investor outside of China can look into buying this stock? Many thanks!