The Investment Case for Solar, Wind and Batteries

The surge in oil, gas, and coal prices is accelerating demand for solar, wind, batteries and electric vehicles as a means to combat inflation, establish energy independence, and reduce environmental impact. The relative weakness in Chinese renewable energy stocks this year presents an attractive entry point for long-term investors.

2022 has been a rough ride for many investors, unless of course you went all-in on oil and gas stocks at the start of the year. Economic activity has sharply rebounded as vaccines facilitate a return to normal, and it turns out that our cars and planes still use the same kind of fuel as before the pandemic. The supply side has struggled to catch up with demand as persistently low oil prices over the past decade caused many oil producers to curtail capital investment as they switched from growth to survival mode, culminating in a record $100 billion worth of North American oil and gas producers entering bankruptcy during the height of the coronavirus pandemic in 2020. To add more fuel to the fire, the Russian invasion of Ukraine and resulting political fallout constrained a significant source of oil and gas supply to Europe during a seasonal peak in heating demand. As oil ran to prices not seen since 2008 and subsequent inflation and rising interest rates weighed heavily on long-duration growth stocks in the technology sector, oil and gas stocks outperformed the broader S&P 500 by 70% through the first five months of the year.

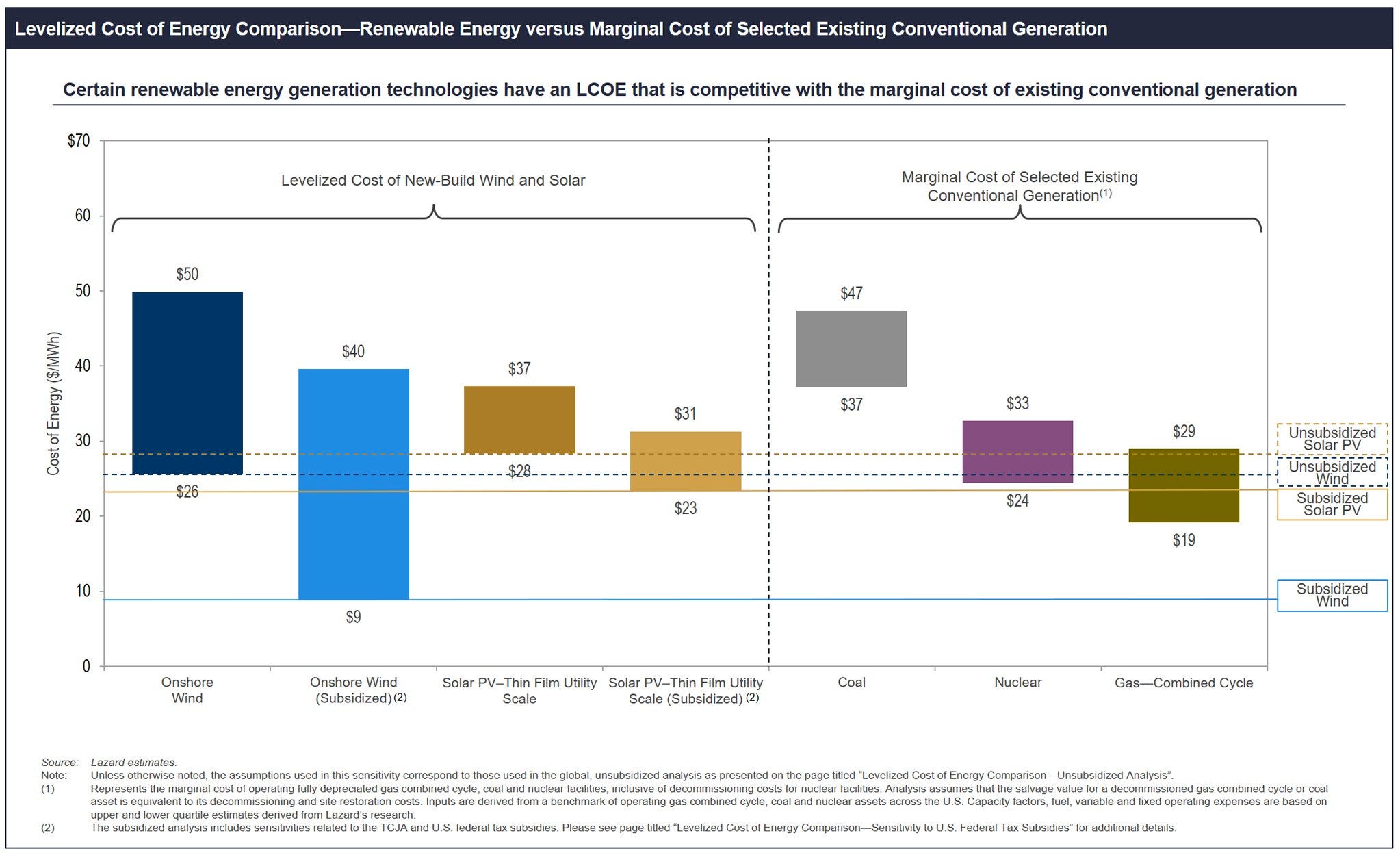

While the market appears to be acting rationally on the surface, it is making one glaring oversight. Renewables have been left out of the rally in the energy sector, as they have been lumped in with other high-growth stocks that have taken a beating due to higher interest rates. This may have made sense in past cycles, as the renewable energy and electric vehicle industries existed on a relatively tiny scale to serve niche markets and were nowhere close to being cost-competitive with fossil fuels for mass consumption. However, this is rapidly changing as renewable technologies follow their learning (cost) curves, meaning they become cheaper to produce at a predictable rate as more units are produced, which drives a virtuous cycle of lower prices, more demand, and more production. Fossil fuels, on the other hand, do not benefit from a learning curve, in part due to the maturity of combustion engine and power plant technologies, as well as a rising cost of extraction over time as the world’s cheapest resources tend to be discovered and depleted first. Even before the recent surge in input prices, this dynamic led solar and wind to leapfrog fossil fuels to become the cheapest source of electricity from new power plants over the past decade:

Price declines for renewables have temporarily gone in reverse as the industry contends with rising prices of most input materials, such as polysilicon used for solar wafer production, the steel used for wind turbines, and various minerals that go into lithium-ion batteries. For solar and wind, prices are back to 2018 levels, while lithium-ion batteries have risen back to 2020 levels. As fossil fuel prices have now risen to 2x-4x 2018 levels, higher prices have not had any chilling effect on demand for renewables and electric vehicles. An updated LCOE (levelized cost of energy) analysis from Lazard in October 2021 concluded that unsubsidized new-build wind and solar projects have already fallen below the cost of operating existing coal plants, and are competitive with existing gas plants. Since then, the price of coal has risen 100% and oil and gas have risen approximately 50%, while the cost of solar modules has been relatively flat. The difference in cost is perhaps most apparent in the Australian power market, where customers of the coal-heavy New South Wales and Queensland grids are contending with larger price increases than in South Australia, where the renewable mix is higher.

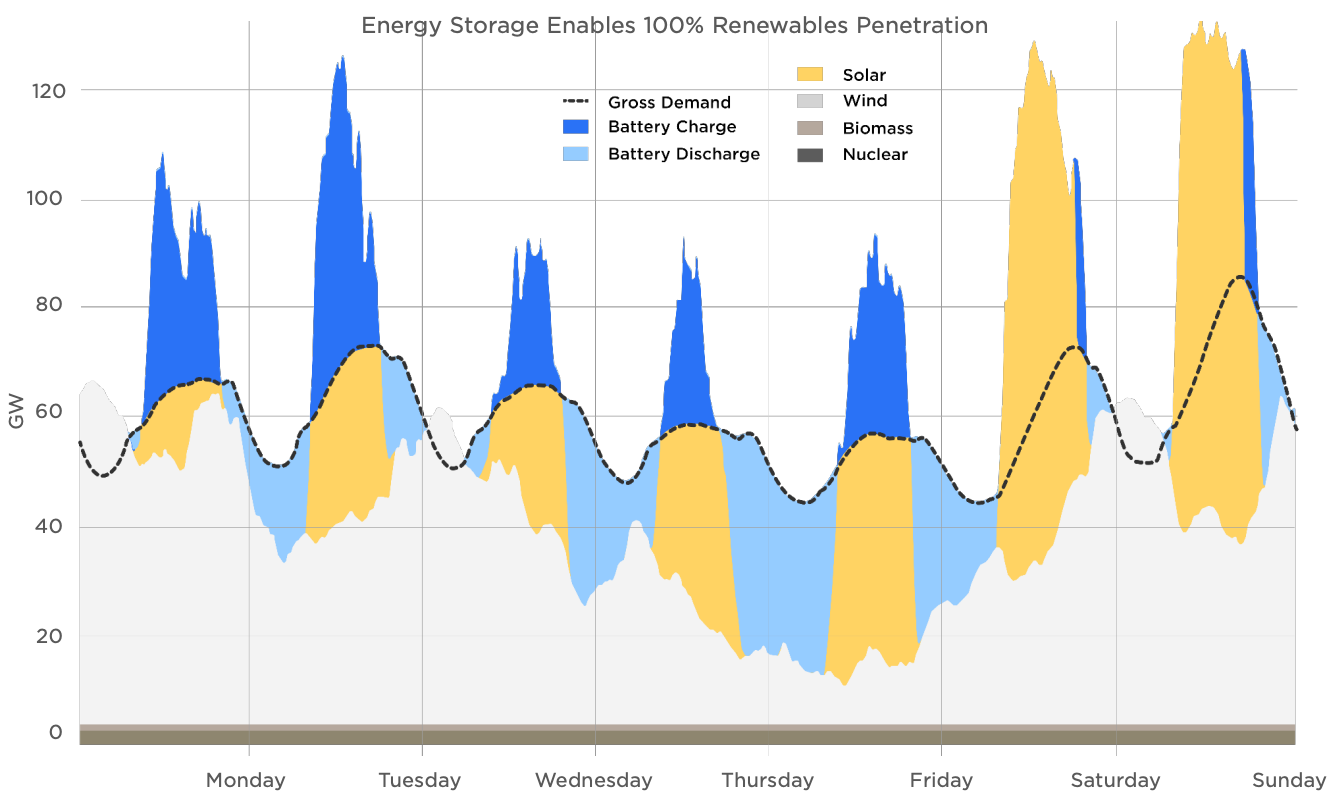

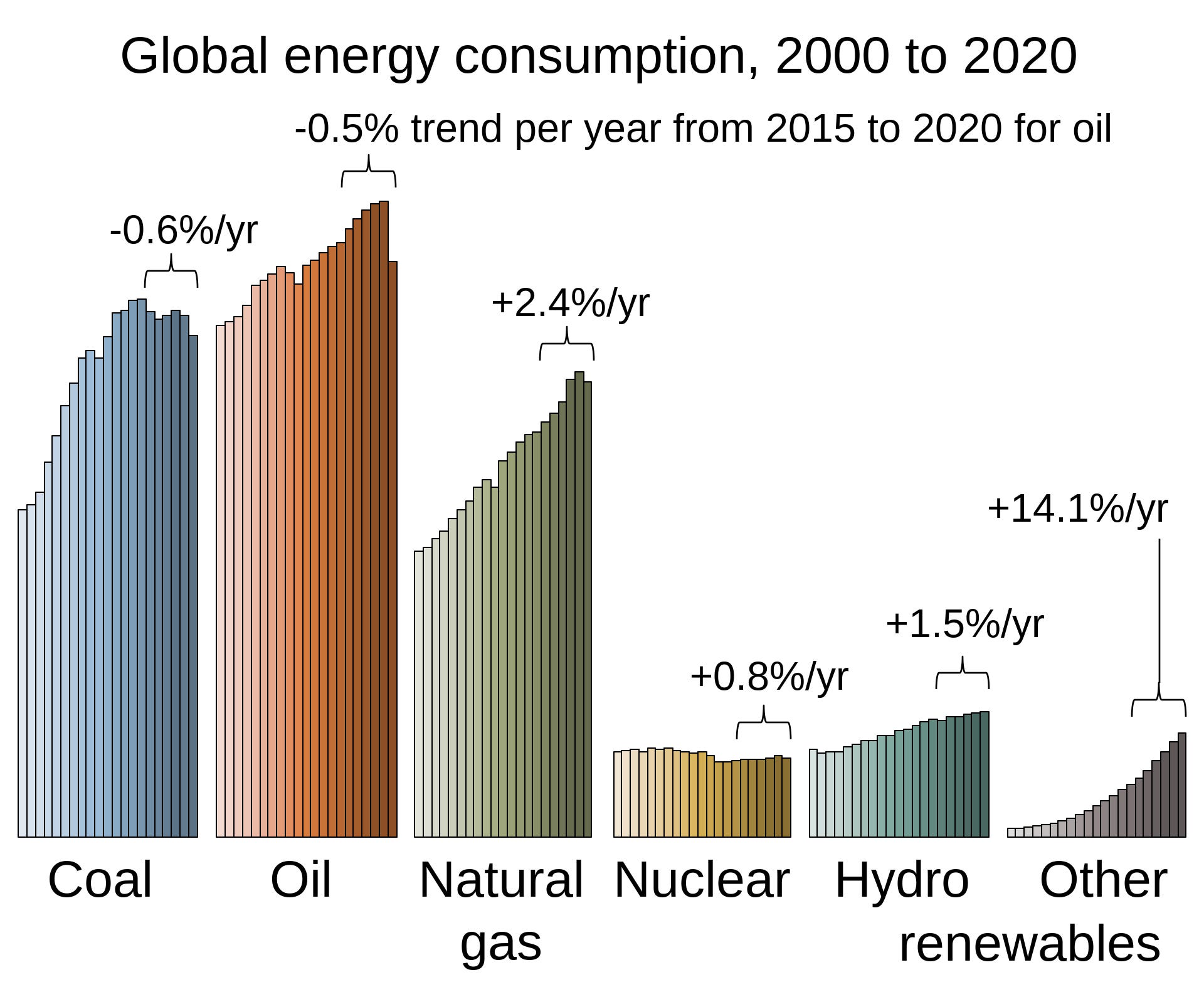

Governments, utilities, and homeowners have taken note; in 2021, 85% of new power generation capacity in the U.S. came from solar and wind, but there is still a long way to go with only ~5% of the world’s energy consumption generated from non-hydro renewable sources. The debate has now moved on to whether renewables can fully replace the existing grid. One argument against the full adoption of renewables is that solar and wind are inadequate to meet our energy needs at certain times of the day or night, as the sun doesn’t always shine and the wind doesn’t always blow. With the advent of grid-scale lithium-ion battery storage, however, it is now possible to meet energy demand entirely from a 100% renewable grid system. Tesla demonstrated the feasibility of such a system in their 2021 Impact Report.

In the coming years, new gas peaker plants will likely be phased out as production of lithium-ion grid storage is scaled up, given the superior economics of lithium-ion batteries even at current prices, which are still improving rapidly along their own learning curve. Lithium-ion battery pack prices have fallen 81% since 2013 on the back of consistent improvements in energy density, battery chemistry, and manufacturing efficiency. Lower battery prices have made electric vehicles and energy storage solutions commercially viable for the first time in history, and overwhelming demand for these products has led to aggressive capacity expansion targets from the major cell manufacturers.

In past oil shocks, consumers either had to bite the bullet and absorb higher prices or use less fuel, behaviors that typically trigger a recession. This time around they have a third option that enables them to maintain their current lifestyle, cut fossil fuel use entirely, and free up more discretionary income over the long run. In the U.S., homeowners can recoup their investment in rooftop solar panels in an average of eight years, while the panel lives continue to lengthen as technology improves, with some warranties going up to 40 years. For those in the market for a new car, it is a financial no-brainer to pair rooftop solar with an electric vehicle, which can already afford buyers a lower total cost of ownership than equivalent ICE models due to lower fuel, maintenance and depreciation costs, making up for a higher price tag. As battery production scaled to catch up to the surge in demand, global EV sales inflected in 2021, growing 108% over 2020:

Despite the attractive economics of renewable and EV technology for consumers and an apparent acceleration in demand and sales as word spreads and production ramps, the typical analyst forecast assumes a sharp moderation in growth in the near term and a very gradual march toward a zero-emission global economy. For example, BloombergNEF, which generally has a bullish long-term view on EV adoption rates, missed 2021 EV volumes by a large margin in May 2021, projecting 4.4 million total BEV and PHEV sales (vs. actual 6.7m). In 2020, BloombergNEF estimated 2025 passenger EV sales of 8.5m, a number that will easily be beaten in 2022. Conversely, an accelerated timeline for renewable and EV adoption will mean long-term forecasts for oil demand could prove to be far too aggressive. Even large integrated oil giants such as Chevron and ExxonMobil could become marginal producers in the future, struggling to contend with a rapidly shrinking market and relentless competition from Saudi Aramco and other low-cost producers in the Middle East who will look to maintain their production levels to fund their government budgets. BloombergNEF’s long-term scenario, which appears to be overly conservative with every passing year, has total oil demand falling by 20mbpd by 2050 from road transport alone (20% of total demand today):

The fundamental flaw in mainstream analyses of the energy market over the past decade is that the cost curves of disruptive technologies are not accounted for at their historical rates of improvement, perhaps because when they are, the logical conclusion about the near future is a radical departure from the present. The nature of exponential compounding can also create a mental roadblock when we are thinking about large numbers that simply don’t seem feasible today. For instance, 476GWh of lithium-ion batteries were shipped in 2021, a 72% increase over the year before. Not many analysts would have stuck their neck out to predict an annual production increase of 200GWh ten years ago when total production was only about 20GWh. Very few today are calling for a 5TWh annual increase in battery production ten years from now, even though we needed it yesterday, as it will take an estimated 300TWh of installed capacity to fully shift the global economy away from fossil fuels.

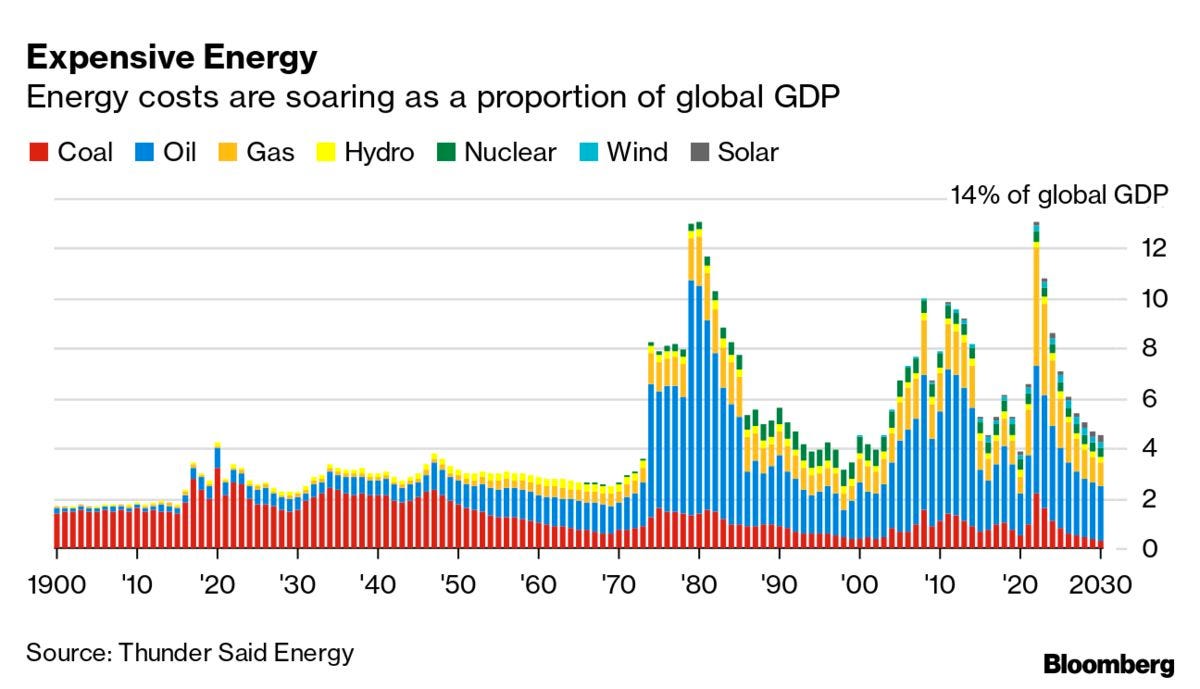

While true that there are numerous engineering problems, logistical hurdles, and material supply bottlenecks to solve, there are significant incentives, financial and otherwise, for our brightest minds to rise to the challenge. In 2022, energy costs are expected to surge to 13% of global GDP, from about 5% in recent years. In other words, the world is now burning $10T on energy annually, up from $4T in recent years. Renewable technology companies have just seen their total addressable market double, raising the urgency for an acceleration of the transition.

The failure of governments and mainstream analysts to grasp the exponential nature of renewable and EV disruption is a golden opportunity for long-term investors with the right mental framework. RethinkX, led by Tony Seba, is one research outfit that has made more accurate predictions over the past decade using technology cost curves as the foundational inputs in their analysis. According to RethinkX analysis, the cost of a 100% Solar/Wind/Battery electrical grid will decline another 75% over the next decade, making renewables not only the cheapest source of new power generation but also cheaper than operating legacy fossil fuel power generation assets by 2030. Such systems will require significantly more nameplate power generation capacity to lessen the need for battery storage. For example, the United States would need 3.3TW to 5.5TW of solar and wind generation capacity to fully replace its 1.1TW electrical grid today, of which only 200GW is currently solar and wind. The world’s ~7.5TW electrical grid added roughly 250GW of new solar and wind capacity in 2020, with a cumulative installed capacity that will likely cross 2TW in 2022. Assuming annual solar and wind deployments continue to expand at their historical growth rates of 23% and 12% respectively, the entire world would be able to adopt a 100% SWB electrical grid by 2040, or shortly thereafter:

In this scenario, annual solar PV deployment would exceed 1TW by 2030, and continue to grow toward 10TW by 2040. This is similar to what major players in the solar industry are communicating today, but a radical departure from the 2050 Net Zero targets set by the International Energy Agency, which works with governments around the world to shape energy policies. In the IEA’s “aggressive” scenario, annual solar PV installations reach 630 GWh in 2030 and remain there until 2050. Likewise, wind capacity additions peak in 2030:

While 10TW of new annual solar capacity additions may feel like overdoing it a bit based on today’s economy and today’s technology, there are strong market forces pushing us in that direction. The renewable energy and EV markets are reasonably fragmented and competitive, with long-term profitability and survival hinging on lowering costs and increasing volumes. Today’s new power generation market is just the tip of the iceberg of total energy demand, and as supply increases and prices fall relative to fossil fuels, eventually all of that demand can be addressed by cheaper renewables. During peak generation hours, 100% SWB systems would also have the added benefit of generating extremely cheap excess power, which could be used by businesses to attract customers (free EV charging) or governments to attract investment and employment from energy-intensive industries (manufacturing, etc.). As the world finds new ways to utilize cheap power, there will be increased competition to deploy as much renewable energy as possible to drive economic growth. At the same time, a rapid decline in fossil fuel use could cause operating costs per unit of energy to spike to uneconomic levels (see current coal prices), accelerating the need to phase out legacy power generation infrastructure. In the medium-term, these forces could drive elevated growth rates for renewable and EV sales above historical norms, with growth moderating as 100% SWB is achieved.

How can investors gain direct exposure to this theme? The most obvious household name is Tesla, which is worth studying to understand what the blueprint of success may be in other industries. Tesla is poised to be a long-term winner in electric vehicles given its cost and scale advantage in manufacturing and its pricing power stemming from superior energy efficiency and user experience. These advantages can be traced back to the company’s pursuit of vertical integration across hardware, software, and services. Thanks to cost advantages and pricing power, Tesla enjoys the highest gross margins of any major automotive OEM and is poised to capture the lion’s share of the EV industry’s profit going forward with only ~20% share of industry volumes, a dynamic similar to what Apple enjoys in the smartphone market today. At maturity, a majority of Tesla’s profits will come from recurring software services, a business model that deserves a significantly higher valuation than the legacy automotive OEM model. I won’t spend too much time writing about this one as there is a lot of quality research out there on Tesla already; if you are new to the idea, this recent write-up is a good place as any to start.

For those who have an Asian mandate or wish to diversify their portfolio exposure across other winners in the space, a good place to start learning is by studying the global leaders in solar panels, wind turbines, and batteries on the Mainland Chinese exchanges, which foreign investors can access via the HKEX Stock Connect. The common theme of vertical integration, cost and scale advantages, and more efficient products gives these companies a superior margin profile and higher return on invested capital than their peers, positioning them for a long runway of rapid earnings growth as they ride the wave of 100% SWB adoption. The three companies I will highlight in future articles grew revenue between 40% and 70% annually over the past five years while maintaining best-in-class profit margins, and now that the stocks have taken a breather this year they appear reasonably priced on next year’s expected earnings.

Be sure to subscribe, spread the word, and stay tuned as we explore this corner of the markets to uncover winning stocks!