Can Tesla Compete in the Chinese Robotaxi Market? - Part 2

Tesla Robotaxi Model, Chinese Robotaxi Players, EV Manufacturers, and Chipmakers

This content was originally sent to paid subscribers in August. Please note that I will be posting far less frequently going forward, due to ongoing consulting engagements. Paid subscriptions have been paused for the time being.

The Money Corner Tesla Robotaxi Model

Tesla’s Production Goals

On Battery Day in 2020, Musk stated an aspirational goal of producing 20 million vehicles annually by 2030. At Tesla’s recent shareholder meeting, Musk guided that Tesla would exit 2022 at a 2 million vehicle annual run rate and said he would be surprised if Tesla did not produce more than 100 million vehicles within the next ten years. Tesla’s production track record to date gives us little reason to doubt these ambitions. With production still growing about 50% annually at scale, two new factories coming online in Austin and Berlin, and operations still expanding quickly in Shanghai, Tesla is actually tracking ahead of this long-term goal. Tesla’s factories today could eventually ramp to about 4 million annual units, and planned factories that will start production later in the decade should deliver further incremental production efficiencies. The primary constraint will be raw materials for batteries; Tesla’s plan to address this challenge has been covered extensively here. Wall Street has chosen to take this guidance with an enormous grain of salt:

With 3 million Tesla vehicles on the road today, 100 million vehicles will be a cumulative doubling of production by about five times. Tesla unit production costs to date have fallen by about 15% for every doubling of cumulative production, which has closely tracked a similar learning curve, seen with the Ford Model T a hundred years ago. If “Wright’s Law” holds for Tesla, the average production cost of a Model 3/Y could fall to about $15,000 in about ten years. Regulatory approval of FSD and robotaxis could drop costs further, eliminating the need for parts such as pedals, mirrors, steering wheels, and steering columns.

Value of FSD Software

At the same time, Tesla’s lead in developing FSD will keep prices high. Approval for use with no driver will make it possible for a two or three-car household to become a one-car household, and the potential to add the car to the Tesla Network (think AirBnB meets Uber) and generate additional revenue while not in use would also significantly increase the value of the car without an increase in cost. A typical car is used about 12 hours per week; increasing utilization to 60 hours per week via autonomy would theoretically increase its value by 400%.

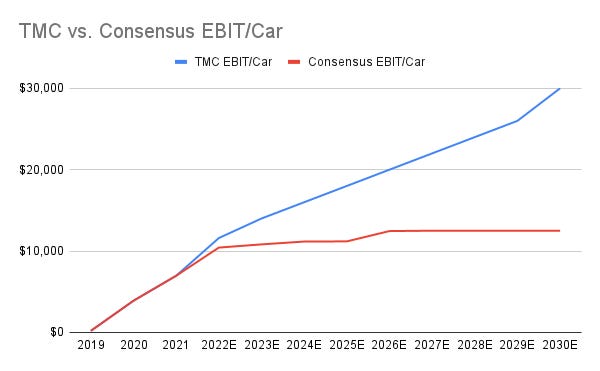

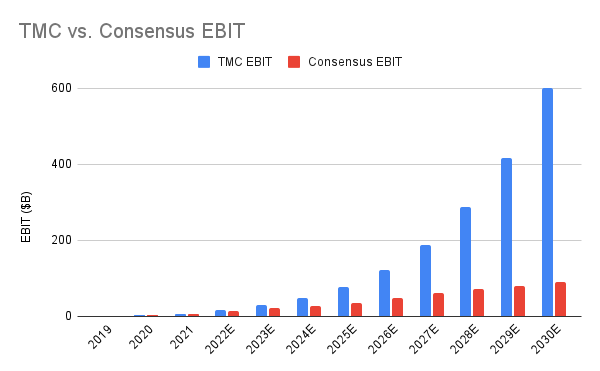

The future financial impact of FSD is very difficult to accurately model because 1) nothing has ever happened like this before and 2) it is anybody’s guess what the revenue mix will be between company-owned robotaxis, FSD software packages, subscriptions, or usage-based fees. Wall Street has boldly risen to the challenge and collectively decided not to model any value for autonomy at all. Analysts are not modeling any significant further increase in EBIT per car through 2030. I think a reasonable base case is that EBIT per car will roughly triple again by the end of the decade, driven by lower manufacturing and operating costs per car (less than $20k) and the increasing value of FSD software, driving higher prices and adoption rates.

Combining our annual production expectations with our rough estimates of what FSD could be worth gets us a much higher EBIT estimate than the analyst consensus toward the end of the decade:

Assuming a tax rate of 20%, our estimate implies the current share price is trading on less than 2x 2030 earnings with ~44% growth in 2030, compared to analyst estimates of 13x 2030 earnings with ~12% growth. Tesla is fairly valued on consensus numbers, but extremely undervalued if Tesla delivers on their production goals and FSD. However, this model is too conservative if we consider the implications of solving FSD.

Robotaxi Riches

The most obvious opportunity is to create a robotaxi network, which Musk envisions will be a mix of AirBnB and Uber. Tesla would take a cut of revenue generated by car owners operating on the network, as well as deploy company-owned robotaxis as necessary. Musk has been widely ridiculed for the statements he made on Autonomy Day about Tesla’s robotaxi network, primarily because the timelines have proven to be way too aggressive. Now that we are on the cusp of the widespread release of FSD Beta and the system is poised to improve exponentially, it is worth revisiting these economics again. A Model 3 robotaxi that costs $38,000 to build (this has dropped since) charging $1 per mile would generate an annual gross profit of $30,000, assuming a 50% utilization rate. With a 1 million-mile battery life, the NPV of a robotaxi works out to about $200k.

The size of the ride-hailing market in the United States in a normal economic environment is about $70 billion. However, this market is severely limited by high prices (~$2 per mile) in relation to personal car ownership (~$0.50 per mile). The market for Tesla robotaxi services will be much larger than the current ride-hailing market, as the price per mile will be about $1. At this price, robotaxis will be competitive with car rentals and begin to be competitive with personal car ownership due to added convenience (no need to find and pay for parking, maintain the vehicle, buy insurance, etc.). With no other company in North America able to compete on operating cost, network scale, and geographic coverage, Tesla will have a huge runway for deploying its own robotaxis. My model below assumes roughly 60% of total production will be dedicated to robotaxi toward the end of the decade, with a total fleet of 35 million company-owned robotaxis earning $30,000 gross profit annually by 2030:

There are other monetizable applications of FSD that are not included in this model, such as Tesla Bot, a company-operated logistics network, and AI training as a service with Dojo. If Tesla can execute on scaling the promise of its technology, as it has in the past, the next decade will be a very fun ride for Tesla shareholders.

Chinese Autonomy Landscape

Understanding the implications of what Tesla is doing with FSD in the U.S. now is critical for properly analyzing the Chinese autonomous driving landscape. Given Musk’s recent comments about Chinese EV competition taking share globally and the necessity of autonomy for EV makers to remain competitive, it would stand to reason that he believes the Chinese automakers are the most globally competitive in this regard as well. The rest of this article will highlight the main competitors in China and their approaches to solving the problem, giving readers the tools to determine whether or not Tesla’s lead in the U.S. market is transferrable to China, how large the potential Chinese robotaxi market could be, and if there is a better way to invest directly in the Chinese market.

The Chinese landscape can be divided into two main categories, the pureplay robotaxi players similar to Waymo/Cruise and the EV manufacturers developing ADAS systems similar to Tesla. The leading robotaxi players are $BIDU Baidu Apollo and Pony.ai. The leading EV manufacturers are $NIO Nio, $XPEV Xiaopeng, $LI Li Auto, and $002594 BYD. It should be noted that the robust third-party EV supply chain in China makes it easier for new entrants to survive than in the U.S. or Europe, so it is more likely that new entrants emerge in this market over time. For example, homegrown tech giants Huawei and Xiaomi have both recently thrown their hats in the ring to develop self-driving technology. The barriers to entering the market with a working prototype using HD maps and LIDAR are relatively low; as the market develops, the barriers to entry will be operating cost and scale.

Baidu

Baidu is best known for operating China’s leading search engine, although it’s a far cry from being the “Google of China.” Like Google, Baidu uses some of the profits from its core advertising business to fund a self-driving arm in start-up mode, but unlike Google, Baidu has far less cash flow to burn. In 2021, Baidu generated about 2% of the level of Google’s operating income on about 8% of its revenue. However, Baidu is betting big on its self-driving ambitions, with an estimated ~$10B of R&D going into the venture since 2015.

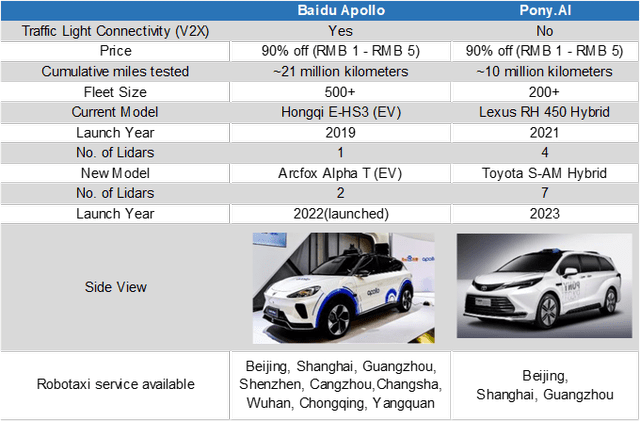

Like Waymo, Baidu’s Apollo uses LIDAR and HD maps. Also like Waymo, Apollo skipped straight to robotaxis and appears to be ahead of the pack in terms of official testing miles and regulatory permits. Apollo Go has given more than 1 million rides to date and is operating in 10 major cities, with plans to expand to 65 cities by 2025 and 100 cities by 2030. The 5th generation Apollo Moon has a production cost of $72k, which Baidu claims is the lowest in China (and much lower than the $200k rigs at Cruise and Waymo). Baidu’s location in China, the leading EV manufacturing hub of the world, presents it with the opportunity to vertically integrate into manufacturing itself, something Waymo has not attempted in the U.S. Baidu will partner with Geely to manufacture the Apollo RT6, which will have a removable steering wheel and integrate 8 LIDAR sensors, 18 radars, and 12 cameras into the roof. Baidu plans to roll out 100,000 of these vehicles within the next few years.

Baidu’s JV with Geely has also revealed a consumer model, Jidu ROBO-01, which is slated for production in 2023 and will be priced very competitively, around $30k. Like the RT6, the ROBO-01 will have a suite of 31 integrated sensors and an autonomous driving system powered by two Nvidia Orin X chips. The JV will introduce a second model in 2024 and aims to produce 800,000 cars annually by 2028. Baidu CEO Robin Li claims that Jidu will be one generation ahead of Tesla, saying, “Our understanding of smart vehicles is that being electric is the semi-final while being intelligent is the final.”

This comment is telling because it is a leader in the Chinese self-driving space acknowledging Tesla as its main competition. The Chinese competition understands that denial is not a viable strategy, as we often see with legacy automakers. Baidu is certainly way ahead of where Waymo and Cruise are today in terms of validation, permitting, vertical integration, cost reduction, plans for mass production, and extension of their technology into the consumer space. However, the elephant in the room remains the difficulty of scaling an HD map and LIDAR approach beyond a geofenced area of operation. It is highly unlikely that the ROBO-01 will be able to drive everywhere in China, on both highways, city streets, and village roads. The use of so many different types of sensors is more of a negative than a positive; Tesla dropped forward-facing radar last year to go all-in on pure vision after having trouble with sensor fusion. If Tesla had problems incorporating just one radar into its vision system, Baidu will definitely run into problems with 5 radars, 2 LIDAR, and 12 cameras.

Pony.AI

Pony.AI, co-founded by a former Waymo employee and a former Baidu employee and based in Fremont, California, is currently the only other robotaxi operator in China that can charge fees for robotaxi services. Baidu seems to be comfortably in the lead, with cheaper, more efficient EV models, a larger fleet, more testing miles, and more permits. Pony.AI’s strategy to use customized ICE and hybrid models likely stems from its financial backing from Toyota, which is notably behind in the transition to EVs. Given the Company’s Waymo pedigree, an even heavier reliance on LIDAR than Baidu, dependence on Nvidia chips, and a partnership with slow-moving legacy auto giant Toyota, their positioning is not great to win the market in the long run. However, the Toyota connection could allow them to scale up very quickly, perhaps if Toyota realized autonomy was their lifeline from falling behind in the EV transition and acquired the company outright.

Chinese Robotaxi Economics

Robotaxi economics are more challenging in China, as normal taxis are much cheaper than in the U.S. or Europe due to lower driver wages. Chinese drivers earn on average ¥8400 ($1230) per month, about half of what the average driver earns in the U.S. Tesla’s theoretical fares of $1 per mile that would undercut average Uber prices in North America by 50% would not be competitive with Chinese taxis, even in the most expensive cities.

Pony.ai has disclosed that its robotaxi rides cost ¥2.6 per km ($0.61 per mile) in off-peak hours and ¥3 per km ($0.71 per mile) during peak hours, which is comparable to traditional taxi pricing in Beijing. Baidu’s CEO has guided that its robotaxi pricing would eventually be half of that of a taxi, suggesting a future fare of ¥1.6 to ¥2.2 per km ($0.38 to$0.51 per mile).

With the starting manufacturing cost of the Apollo RT6 approaching that of a Model 3, Baidu could be competitive on operating expense per mile with Tesla, but operating margins will be much lower than Tesla in North America. Their ringfenced area of operation will also limit their ability to scale and deliver a service that can truly compete with taxis that can go anywhere. It is unclear to me if Baidu will be able to profitably scale fast enough for the robotaxi business to generate an outsized return for shareholders buying in at the current market cap of ~$50 billion. 100,000 cars operating in 100 cities by 2030 could generate roughly $1 billion of gross profit, which might barely break even on operating profit, but perhaps these numbers are too conservative.

The challenging economics of robotaxis in China could prompt an alternate strategy from Tesla in this market. Rather than trying to compete with the cost of personal car ownership, Tesla could leverage its brand in China to position itself as a more premium service. Company-owned robotaxis could focus on long-distance trips that Baidu and Pony.AI would be unable to make. Perhaps Tesla will lean more on private car sales in China, as they can recoup their manufacturing cost immediately, and then monetize their autonomous software primarily through customers adding their cars to the Tesla Network.

EV Manufacturers - Tesla, Nio, Xpeng, Li Auto, Zeekr, BYD

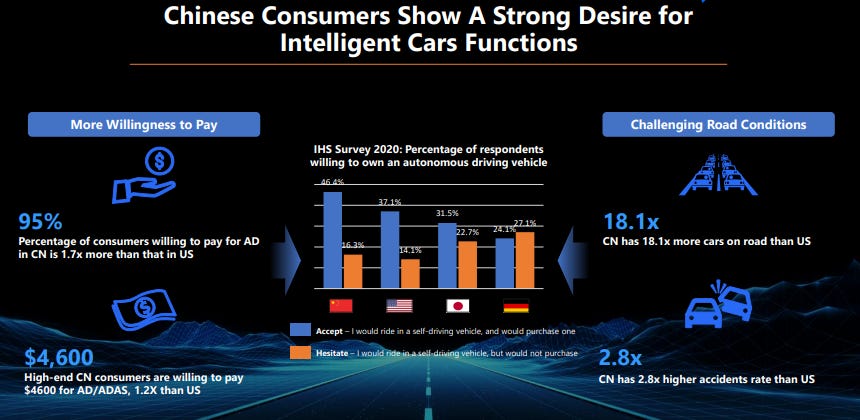

Interestingly, whereas Chinese consumers would expect far cheaper robotaxi rides than U.S. consumers, they are actually willing to pay 20% more for high-end ADAS in their personal car:

FSD Beta is not rolled out in China yet, but Enhanced Autopilot was launched there in June 2022. In China, Enhanced Autopilot is a ¥32,000 ($4,800) option that included Navigate on Autopilot, Auto Lane Change, Autopark, Summon, and Smart Summon capabilities. All cars include Basic Autopilot free of charge, which consists of adaptive cruise control, emergency braking, blind-spot monitoring, and lane-keeping assistance on the highway. According to expert Tesla car-counter @TroyTeslike, take rates have been exceptionally low in China for FSD, which promises the ability to navigate city streets in the future.

I can think of several reasons for the low take rate of FSD in China. For one, the price of a Tesla is already at a significant premium to competing EVs in the Chinese market, and new buyers may feel a bit too tapped out to splurge on a feature that is not yet available. Owners could be interested in the feature but holding out for a better deal, which tends to occur more often in the Chinese market than the rest of the world. This month, Tesla China announced a promotion for owners to upgrade to FSD at a 50% discount. Perhaps this is a signal that FSD Beta will reach China soon.

While no EV manufacturer has released any software with similar capabilities to FSD Beta on city streets, Tesla faces stiff competition from domestic manufacturers on the highways. Tesla’s Navigate on Autopilot guides a car from a highway’s on-ramp to off-ramp, including suggesting and making lane changes, navigating highway interchanges, and taking exits. Nio became the second automaker to deliver this active guidance feature “Navigate on Pilot” in October 2020, followed by XPeng’s Highway Navigation Guided Pilot in January 2021 and Li Auto’s Navigate on Autopilot (bonus points for originality) in December 2021. Nio, Xpeng, and Li Auto have all followed Tesla’s footsteps in developing the software in-house, but they still rely on third parties for hardware and HD maps.

Tesla’s self-developed FSD chip is a clear advantage in terms of performance, and the additional compute power gives it room to take on the task of city street navigation in the future, while the three challengers rely on third-party vendors and would likely need a hardware upgrade (roughly 50 TOPS needed to tackle autonomous driving). Older models do not have LIDAR, but all three of the Chinese challengers listed here have announced plans to add LIDAR to future models, which could add expense and complication to the software stack from sensor fusion. The challengers all use millimeter wave radar, which Tesla has dropped going forward.

However, despite Tesla’s decisive hardware advantage, the challengers have closed the gap with their software, tailored to Chinese road conditions and driving behavior. According to 42How, a Chinese media outlet focused on autonomous driving, the challengers actually deliver a better driver experience on Chinese highways:

“As the top dog, Tesla outperforms the others in basic capabilities, but it still doesn’t know enough about the Chinese road conditions. The navigation is not user-friendly, deceleration comes in late upon entering the ramp, the speed doesn’t come up when exiting the ramp, etc. Those are the issues that Tesla needs to solve urgently. Although Tesla is the first to release this feature, clearly the NEV startups in China have come from behind.”

In 42How’s most recent comparison of the four Navigate on Autopilot contenders, the Xpeng P7 came out on top. This is a pretty impressive achievement for Alibaba-backed Xpeng, which was once accused by Tesla of stealing the Autopilot source code but ultimately cleared of the allegations by a third-party investigation. Last month, Xpeng gave us a glimpse of its Navigation Guided Pilot for city streets, which will be a competitor to FSD. Similar to Tesla, Xpeng and Alibaba Cloud have set up China’s largest cloud-based computer center for training machine learning models for autonomous driving. Xpeng is targeting an L4 solution, and with an entry-level price of ¥250,000, it should be very competitive. However, Xpeng’s solution also uses HD maps and LIDAR, so the system will initially only work in select Chinese cities, and there are no immediate plans to develop the system for city streets outside of China.

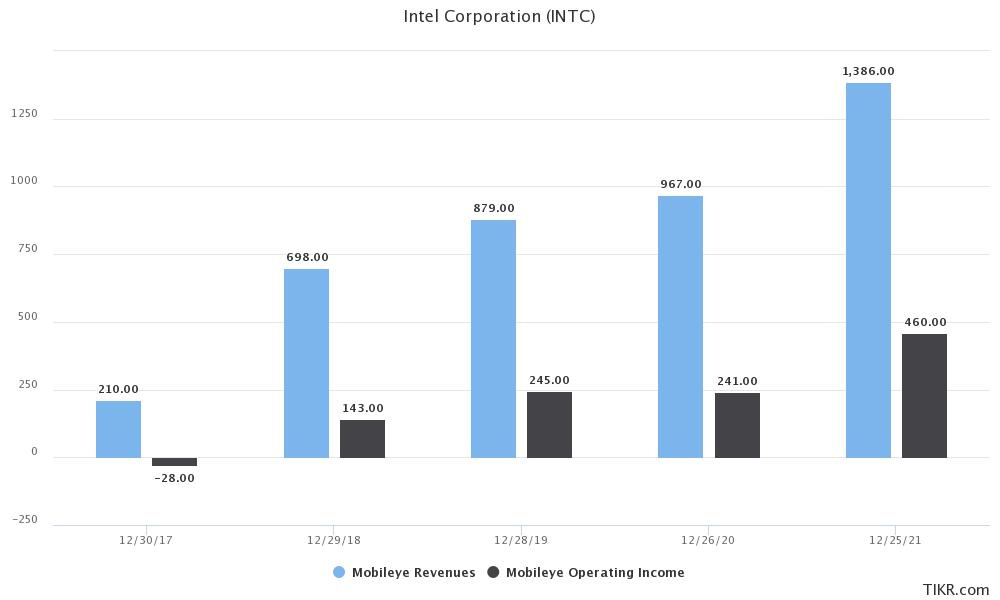

Tencent-backed Nio also had a strong showing despite an aging hardware platform, and the Company’s upcoming ET7 platform could usher in their next wave of autonomous development (again, with HD maps and LIDAR). Nio’s partnership with Mobileye is planned to extend to the robotaxi market; in 2019 Nio agreed to engineer and mass-produce a self-driving system built on Mobileye’s L4 Autonomous Vehicle kit. I think the future of this partnership is uncertain, given questions around how the value of a robotaxi would be shared. Nio has since relaunched its own L4 driving technology development. In general, Mobileye may struggle to collect the real-world data needed to train its system through its OEM partners, as they move to protect their own valuable data streams in hopes of creating their own autonomous platforms. Mobileye’s partnership with upstart Chinese EV brand Zeekr to deploy a new pure vision-based platform may be their best way forward in China, as Mobileye’s parent Intel has invested in Zeekr to ensure proper incentives for collaboration.

Chipmakers - Nvidia, Mobileye, Horizon Robotics

The leading Chinese EV manufacturers have made promising progress with their autonomous capabilities, but achieving scale, profitability, and global relevance are still significant challenges. The market is crowded and highly competitive, and Nio, Xpeng, and Li Auto are still loss-making. On the other hand, the chipmakers that the automotive OEMs are reliant on to power their self-driving ambitions are already profitable and positioned to grow, regardless of which of their customers wins or loses. Barriers to entry to chip design and production are relatively high, and there are only a handful of leading players. $NVDA is a juggernaut in the space, but only 2% of its revenue comes from automotive. The anticipated Mobileye IPO will give investors a way to invest directly in chips for driving. Mobileye is currently generating more than twice the amount of $NVDA’s automotive revenue with attractive growth and operating margins, but we will not have a geographic breakdown until it goes public:

Following this logic, Horizon Robotics stands out as perhaps the best way to invest directly in the Chinese autonomous driving market. Founded in 2015 by Kai Yu, the founder of Baidu’s Autonomous Driving and Deep Learning units, Horizon Robotics is uniquely positioned as a Chinese company primarily focused on developing the neural net processing chip (BPU - Brain Processing Unit) specifically for autonomous driving. The chips are compatible with various HD map services and sensor suites, and besides supplying Li Auto, the Company supplies a number of Chinese and foreign OEMs. The Company recently entered into an agreement to supply their next-generation chips to BYD, the world’s leading NEV manufacturer (#2 in BEVs after Tesla). The Journey 5 AI Processor will offer 128 TOPS of processing power, exceeding the current generation of Tesla’s FSD chip (although this is now 3+ years old). Horizon Robotics is still private, attracting investment from major industry players BYD, CATL, and Intel, as well as high-profile institutional investors Hillhouse, Baillie Gifford, and Sequoia. The rest of us may get a chance to invest soon, as the Company is considering an IPO in the Hong Kong market, possibly within the next year.

Summary

China is a hypercompetitive battleground for autonomous vehicle development, with robust ecosystems for EV production, autonomous hardware and software development, eager consumers, and progressive regulators. Tesla is unique in that its autonomous software has not been developed specifically for the Chinese market; its vision-based approach that does not rely on HD maps is being developed in California and exported to the world. The fact that Tesla’s Autopilot works in China at all is a remarkable achievement and validation of Tesla’s differentiated approach to self-driving, but to remain competitive in the Chinese market it may need to calibrate the system to adapt to local driving behavior.

For now, the Chinese players are rapidly advancing their capabilities in the domestic market, but they do not appear to be developing self-driving systems that are exportable to other markets. Approaches using HD maps and LIDAR will be challenging to scale to true autonomy. Tesla has a big resource advantage over the leading Chinese robotaxi and ADAS players, with annual profits exceeding $10 billion and production reaching 2 million units annually by the end of this year. Thin margins and a high probability of failure will not stop Chinese entrepreneurs from competing fiercely, but investors may be wise to stick to companies that others will have to rely on in order to stay in the fight. Horizon Robotics, once public and if listed in its home market, will be worth diving into.

The one topic I have not covered, which may warrant its own post in the future, is regulatory risk. Tesla is the only foreign automaker that was able to make a deal with the Chinese government to retain 100% direct ownership in their Chinese operations. The government made an exception for Tesla due to the importance of developing the EV sector and reducing China’s reliance on fossil fuels. This move has paid off in a big way so far, as the Chinese have been able to build out the world’s leading battery and EV manufacturing ecosystem, enabling the rise of some of the world’s leading companies in EV and renewable technology. Automating electric vehicles will have a major impact on emissions reductions and curtailing fossil fuel use, as it enables a faster phaseout of the existing ICE fleet. However, if robotaxis become a winner-take-all business due to the importance of network effects, Tesla will have to make compromises to avoid the ire of the Chinese regulators. However, this is more of a reason to avoid the U.S.-listed Chinese companies with VIE structures in the space, which will eventually be forced to delist and return to the Mainland. Tesla is the only stock mentioned in this article listed in the right place, with no dotted lines in its ownership structure, and if they are barred from competing in the Chinese robotaxi market, at least it’s not critical to long-term shareholder returns.

As it stands, Tesla is still the only automaker that controls the full stack required for autonomous driving. No other company has the combination of its own deeply vertically integrated manufacturing operations, charging network, mobile service delivery network, neural net chip and autonomous hardware suite design, in-house neural net training, and software development. This strategy at scale has the benefit of keeping costs low, user experience high, and margins unbeatable. The market is still deeply underestimating the power of this business model. In other words, Tesla to the moon 🚀

Concise and informative overview. Good work.

Great work! However, I might have different opinions with you. My conclusion is that in China, the leading auto-taxi player will be Baidu who already operates in some area in Beijing and Chongqing. There are three reasons:the first is its close relationship with government, the second is the advanced algorithm proved by DMV data in California and the third is the mapping system(Baidu map). If you check the DMV data, there are one name also stand out which is Apple. As for Tesla, I do not think it has advantage in China for auto-taxi. The advantage is its data. Every Tesla has shadow mode which records the driver's data. They might be able to benefit a lot from becoming a data provider in the future rather than joining the fierce game.